Over the years, we have shared our Legal Weekly Update, highlighting changes in the legal sector, such as global partner movements and promotions. By tracking partner movements week on week, we have been able to collect rich data that enabled us to identify trends and actionable insights for strategic hiring, in both the long and medium term.

One of the most interesting trends we’ve noticed is in the Paris legal sphere, where we’ve seen a flurry of partner movements in dispute resolution and litigation spaces, since 2020. Firms like Dechert and the late Shearman & Sterling were significantly impacted. The exodus of partners from these establishments has reshaped the city’s legal landscape, leading to the formation of boutique firms and attracting talent to others.

Dechert saw several high-profile exits from its litigation team. Notably, partners – including Claudia Annacker, Eduardo Silva Romero, and José Manuel García Represa – exited the firm in favour of forming boutiques focussed on international arbitration and litigation. The departures are said to have been triggered by Dechert’s strategic shift away from international arbitration and toward life sciences, private assets, private capital, and technology. The Paris International Arbitration Group, which was once an integral part of Dechert, disbanded as partners pursued their own paths. We saw the aforementioned Silva Romero lead the founding of Wordstone Dispute Resolution.

Shearman & Sterling mirrored Dechert, losing a number of partners who merged to form Gaillard Banifatemi Shelbaya Disputes, a boutique firm specialising in international arbitration and law. These departures reflect a systematic shift in the legal market, with seasoned practitioners choosing specialised boutique settings.

However, it is important to note that the landscape has shifted significantly since then. Shearman & Sterling merged with Allen & Overy to form A&O Shearman, a global legal powerhouse. This merger represents a countertrend to the boutique model, emphasising scale and geographic reach. While the departure of partners to boutique firms remains a notable trend, the formation of A&O Shearman exemplifies the ongoing consolidation in the legal industry and the various strategies firms are employing to remain competitive. This trend towards global mergers stands in stark contrast to the rise of boutique firms, suggesting that the legal market is simultaneously pulling in two distinct directions: specialisation and consolidation.

This is further exemplified in the expansion of firms like Paul Hastings, which grew by 12 people, adding a new litigation team through the acquisition of Antonin Lévy & Associés’ white-collar and investigations team. This move is said to be part of the firm’s overall global strategy to strengthen its litigation capabilities while enhancing its position in complex international disputes. The addition of the well-regarded Antonin Lévy and his team is expected to attract new clients and reinforce Paul Hastings’ reputation in the Paris legal market.

Squire Patton Boggs and Bryan Cave Leighton Paisner emerged as top firms in attracting partner talent, with Squire Patton Boggs welcoming Sabrina Aïnouz, Jérôme Lehucher, and John Adam, who joined from DWF and Latham & Watkins respectively, reflecting a trend of group moves. Bryan Cave Leighton Paisner also added three partners: Elodie A. Valette Wlodkowski, Jean-Pierre Delvigne, and Philippe Métais, all of whom joined from White & Case. This move coincided with the departure of Nathan Willmott, Bryan Cave Partners’ European head of litigation, to Ashurst.

We also saw Hoche Société d’avocats emerge as an active player in attracting new talent, with Solène Delafond who joined as a partner in the litigations team, bringing expertise in financial, commercial, and corporate disputes to the firm.

It is evident that the Paris legal landscape is undergoing a significant transformation. The rise of boutique firms, sparked by the departure of key partners from established entities, is reshaping the market by offering clients highly specialised legal services. At the same time, the consolidation of major firms, as seen in the formation of A&O Shearman, highlights the ongoing importance of scale and global reach; additionally, firms like Paul Hastings, Squire Patton Boggs, and Bryan Cave Leighton Paisner are actively capitalising on this shifting landscape, expanding their talent pools and service offerings. This heightened competition promises to advantage clients, offering them an expanded array of specialised legal options. As the Parisian legal market continues to evolve, increased specialisation and competition are poised to define its future course.

Megan is a delivery consultant at Fides Search. To find out more, get in touch at: +44(0) 747 130 9526 or megan@fidessearch.com

Throughout 2022, with both specific in-depth analysis of practice areas such as Data Protection, Venture Capital and Investment Funds, and weekly updates on partner moves, we charted a year full of developments in the legal market. This data collection allowed us to inspect certain individual or clusters of moves and reveal particular trends. On a broader level, this analysis will provide insight on the direction the market is moving; and on a micro level, it reveals the opportunities for strategic hiring. In a turbulent time of change – whether that be the swelling of in-demand NQ salaries, or the difficulties presented by the war in Ukraine – it is even more important that we understand the legal market that we work in.

In this article, we have used our weekly updates from 2022, where we reported on a range of moves internationally, therefore it is a snapshot of the market and not the whole.

As we discussed in our last article documenting the war for talent, who will emerge in the best possible position at the end of the year very much determined by “how leadership teams respond, devise, and implement a smart and timely response” to various new issues that arise.

In a change from 2021, we captured fewer moves from the in-house market; only 45 out of our 806 documented partner moves involved in house placements. Following the post-Covid boom in the sector, with in-house working conditions, job security, and swollen salaries increasingly attracting high quality legal talent, it is only natural that hiring would slow sooner or later. It should be recognised that the in-house market makes up for a much smaller percentage of the market than private practice and they are, overall, reported less frequently in the sources we use for our updates.

Moving into 2023, it will be interesting to see how the whole market adapts to sky-high salaries combined with a greater desire for work/life balance. Curiously, a survey conducted in Canada released on the 24th of January, has shown that in-house lawyers are struggling to cope with their increased workloads; 46% of in-house counsels have seen an increase in their work-related stress and anxiety levels in the last year, compared to only 13% who have seen a decrease.

When analysing the private practice moves, we found that often a team of fee-earners will accompany a partner move, particularly if a team of partners move. At times, even a whole practice may be uprooted. In 2022, there were 131 team moves in total, with the highest concentration of those team moves happening in July with 17 moves, despite there being a lower concentration of total moves. Some of the more notable team moves in July were BCLP taking a 4-partner real estate team from DLA Piper in Frankfurt; Dentons taking a 3-partner corporate team from EY in Singapore; Paul Hastings taking a 4-partner finance team from Latham & Watkins in London; and Linklaters with a 3-partner raid on Vinson & Elkins leveraged finance practice. The other most notable moves of the year include a power play from Reed Smith who brought in highly touted New York real estate finance 12 lawyer, 5 partner team from Akerman in February. Ropes & Gray similarly made a statement in April, taking a high level 3-partner private equity team from Fried Frank in London.

There were the highest concentration of partner moves in March (126) and April (104), compared to a much slower November (48) and December (34). It can be extrapolated that this is related to the law-firm bonus structures which are decided at the end of the calendar year and paid out in the first couple of months of the new year.

October was uncharacteristically busy with over 20% more moves than any other month in the second half of the year. October was also busy with promotions, with notable names such as Kirkland & Ellis, White & Case, Covington & Burling all announcing a new cohort of partners. Alongside the cluster of partner promotions, which usually fall closer to the end of the year, 6 firms including Goodwin Procter, White & Case and Freshfields all opened up offices abroad. 58 promotions accompanied Goodwin’s new Singapore office opening.

Some of the biggest headlines come in the area of high-profile team moves. 2022 was no anomaly; lots of prominent moves made headlines throughout the year. Reed Smith was particularly active when it came to high profile moves. In February they brought in the top real estate finance team to their New York office from Akerman. Not long after, however, they lost a senior corporate duo from their German base Frankfurt to rivals McDermott Will & Emery. The two-partner team of Rolf Hunermann and Philip Schmidt have around three decades of combined experience covering a range of issues from domestic and cross-border M&A to ESG considerations and will be a huge loss. McDermott followed up that acquisition with a 4-partner raid on Orrick, Morrison & Foerster and Kirkland & Ellis to construct an extremely competitive real estate platform in New York and Chicago in May. Despite the bold acquisitions, however, McDermott Will & Emery suffered their own setback in the same month, losing 4 corporate partners across their New York and Tel Aviv offices to the fast-growing Greenberg Traurig.

For the past decade, and particularly since the Brexit referendum in 2017, the battle for a spot in the fertile Dublin market has been ongoing. Pinsent Masons opened up first in the wake of Brexit with a Financial Services and Technology-focussed practice – their 4th international office opening in 18 months at the time and were eagerly followed between 2017 and 2019 by Covington & Burling, DLA Piper, Freshfields, Clyde & Co. and Simmons & Simmons – who poached Mason Hayes & Curran’s head of investment funds and financial regulation Fionan Breathnach to lead them out.

In July, Browne Jacobsen opened up their first international office in Dublin with an end-to-end TMT practice. Not only ambitious in their growth, Browne Jacobson became the first law firm in history to top the Social Mobility Employer Index in 2021 – and impressively retained that spot in 2022. The index is the leading authority on social mobility in the workplace and demonstrates Browne Jacobson’s targeted efforts to open up the legal profession to young people of all backgrounds. Addleshaw Goddard launched in Dublin as well through a merger with local firm Eugene F. Collins, and Squire Patton Boggs – poaching Dennis Agnew, the head of transactions at Pinsent Masons – have set a date in 2023 to follow suit. Ropes & Gray have started the new year with purpose as they too opened in Dublin with Competition. There have been repeated whispers in the market that Bird & Bird and Linklaters are contemplating expansion into Dublin as well, so it will be interesting to see how the market continues to develop in 2023.

Potentially one of the most notable moves of the year was a rare Goodwin Proctor raid on Latham’s Santa Monica office, which saw three corporate partners joining the US firm. Goodwin have historically relied on the inward promotion of their own exceptional talent pool, so a 3-partner hire from a globally leading law firm is a clear statement of intent. Latham also lost a 4-partner finance team to Paul Hastings in London – a similarly impactful statement from Paul Hastings as they look to compete with the very top firms.

Cleary Gottlieb is a firm quite similar to Goodwin with regards to their hiring strategy – they also prefer to nurture their homegrown talent rather than rely on lateral hires. Cleary raided Kirkland & Ellis – a firm who has been on their own frenzied hiring spree in 2022 – for 3 employment, litigation and funds partners across their New York Washington and London offices. The Magic Circle firms seem have changed their hiring strategy approach, and are looking to build upon their strength in Europe and look toward the US market. A prime example of these efforts came from the 3-partner finance team that Linklaters took from Alston & Bird in New York. Along with the acquisition of a 3-partner finance team taken from Vinson Elkins for their London office, the moves are a symbol of the recent magic circle firm’s efforts to expand their lateral hire operations.

In Frankfurt specifically, Willkie Farr & Gallagher have been making waves over the past few years, with more than ten partner and counsel hires. In May, Willkie brought in leading capital markets lawyers Simon Weiss and Joseph Marx from McDermott Will & Emery, which has not only boosted their global capital markets platform, but is also a demonstration of the firms continuing investment into the German market.

BCLP – despite having quite a turbulent and unsteady year – brought over a 4-partner real estate team from DLA Piper in July, making a marked investment in the Frankfurt market as well. BCLP has had a difficult start to 2023 as being named “the golden turd”. As they start 2023 with more uncertainty surrounding the environment and their culture, we might expect to see some significant departures from the firm and a shakeup in senior management.

2022 was certainly one of the most interesting years we have kept track of. It is unlikely we will ever see a year with such aggressive salary inflation for NQs again, and in the face of a recession, US firms have demonstrated their impregnable attitude when it comes to hiring. 2023 will be a crucial year to see whether the more ambitious hiring strategy from magic circle firms both internationally and in the UK will see their profits keep pace with top US firms. They can certainly expect the hiring frenzy to roll on. There is a counter-cyclical relationship between transactional and disputes hires, so as we are seeing the transactional market slow, we would expect the disputes market to become more active over the course of 2023.

Last year, we analysed the trends that were taking place in the Venture Capital Transfer Market in London between 2016 and 2020. This year, we wanted to follow up with what we saw take place in 2021. To recap, in our previous analysis, we found that, in general, the amount of lateral hires in the VC sector had been steadily increasing since 2016, as well as the fact that major US law firms were consistently hiring in this space.

DATE

NAME

LEAVING

JOINING

February 2022

Richard Goold

EY

Wilson Sonsini

January 2022

Sarah Melaney

Brown Rudnick

Withers

November 2021

Andrew Cooke

Sherrards Solicitors

Wallace

October 2021

James Lyons

Devonshires

Lawrence Stephens

September 2021

Jon Gill

TLT

Eversheds Sutherland

June 2021

Adrian Rainey

Goodwin Procter

Balderton Capital

May 2021

Alexis Karim

BCLP

DWF

May 2021

Howard Watt

Sheridans

Fladgate

May 2021

Frances Doherty

Dorsey & Witney

Simmons & Simmons

February 2021

Fergus Gallagher

McDermott Will & Emery

Squire Patton Boggs

February 2021

Peter Kohl

Kerman & Kohl

Armstrong Teasdale

January 2021

Erika McIntyre

Withers

Taylor Vinters

January 2021

Galfkos Tombolis

Kemp Little

Deloitte

When comparing our data to our previous findings, we can see that the amount of lateral hiring has continued to increase from 2020 to 2021, following the same route as the previous trends. US and UK firms continue to show a heavy interest in building out their teams as the market is extremely busy and firms want to have the bandwidth to support as many clients as possible as well as appear attractive to prospective clients.

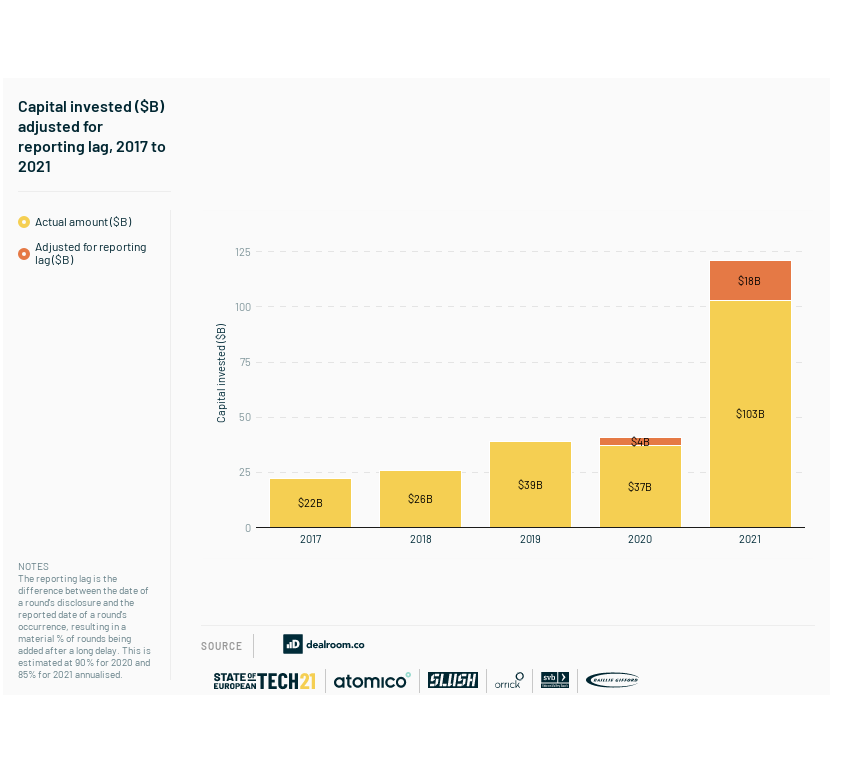

2020 was no doubt a record year in VC investment, with tech firms raising $10.5 billion total, and $249 billion in global funding being invested. 2021 turned out to be no different, with global funding skyrocketing 111% to reach $621 billion. Overall, the amount of capital being invested into tech grew at a steady rate, and seed investors were raising larger and larger funds.

In the UK alone, fintech investment topped $37.3 billion in 2021, a sevenfold increase compared to 2020, with over 600 M&A, VC and private equity deals finalised. London has further cemented itself as the leading European tech hub by way of total capital invested, as London raised $18.4 billion in the first 9 months of 2021, which was 2.6 times more than Berlin in second place. These record level investments have largely been driven by bigger rounds, as rounds over £250 million became 10 times more popular in the last year, and they now represent roughly 40% of the total capital being invested in Europe. In the same vein, rounds below £5 million have stagnated. These are typically at the pre-seed and seed-level of investment, and this is seen as a sign of a “seed squeeze”. However, the volume of investment rounds that are under £5 million is approximately the same as what occurs in the US and it accounts for 33% of all money invested in European tech.

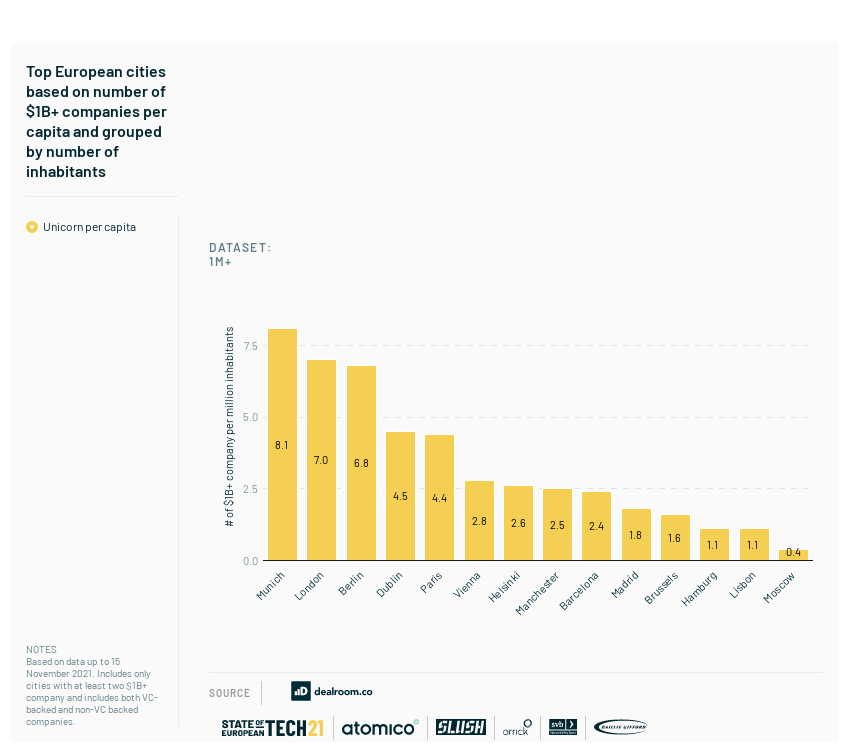

The global unicorn counts has reached an all-time high with 959 companies, a 69% increase from 2020’s 569 unicorns. In Europe, 98 companies rose to the title of unicorn in 2021 alone. The decacorn herd, which is for companies that are worth $10 billion, has also doubled in size, as 26 European companies now hold this status. There is an array of cities in Europe that have become hubs for unicorns. Munich, Stockholm, and Cambridge are leading on ‘unicorn density’, but when looking at cities with a population greater than 1 million, Munich is the clear leader, with London not too far behind them.

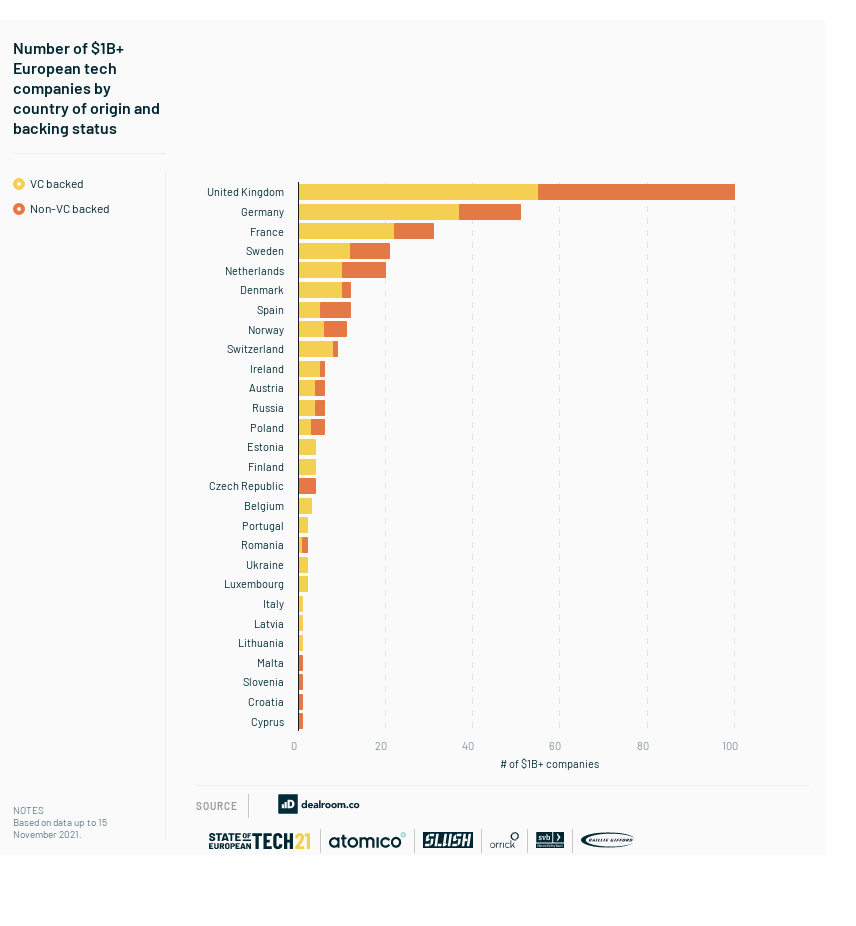

New countries have joined the unicorn this list year, with Latvia and Cyprus being represented by Printful, who raised a $130 million growth rounds in May, and Nexters Group, who reached the status with a $1.9 billion SPAC deal. However, it is clear that, despite the density of unicorns in Munich and Stockholm, the UK is still the leading producer of unicorns, and has reached a momentous milestone having produced 100 unicorns in total.

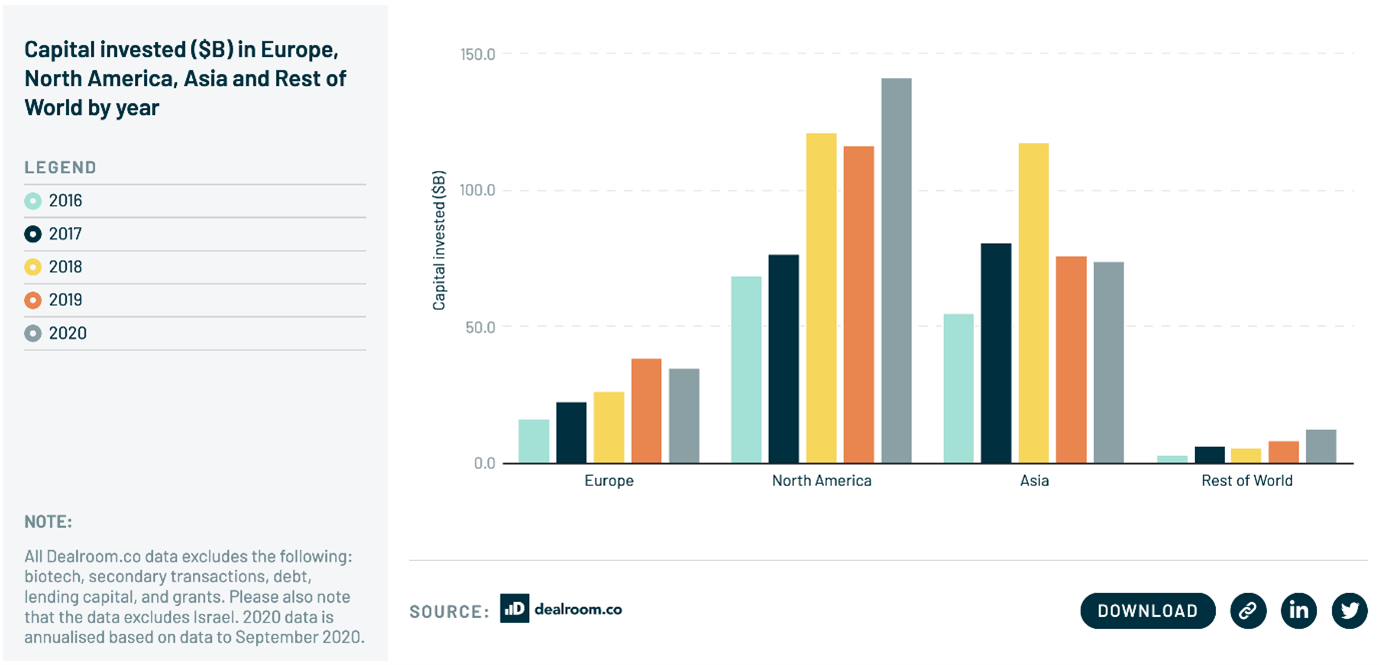

Cross-border investing is also on the rise. While it is common to see US-based investors making investments in Europe, it is now becoming commonplace for European funds to inject capital into the US markets. It is expected that while European VC will “spread out” because physical location matters less and less, “foreign VCs”, namely those from the US, will still be very prevalent, particularly in the later-stage rounds. Christoph Reudig of AlbionVC credits this to the fact that “a lot of European countries don’t have the same kind of cash-rich investors as they do in the US… It takes time for an ecosystem to develop and we’re starting to see local investors exploring [later-stage] opportunities, but in the short term, I don’t think they will be as involved”. European tech itself is reaching unprecedented levels of growth and investment as it is currently on track to break the $100 billion milestone of capital invested in a single year, tripling the amount invested in 2020, so it is clear that these investors are getting involved, and in a few years’ time we will likely see the gap closing in the later-stages. As you can see in the chart below, European technology companies have already made their mark in early-stage funding, with the European share growing at the direct expense of the US – Europe has increased its share of funding by 13%, while the US has decreased by almost 20%. This shows the developing investor desire that will no doubt continue to grow in the amount of late-stage funding that occurs.

Competition is very strong leading to bigger valuations and bigger investments. There will be more emphasis on what additional resources VCs can bring to founders when competing to win deals with a big focus on human capital and talent as well as experience.

There will of course be challenges ahead and there is no surprise that ESG-related goals have come to the forefront of minds, both with start-ups and investors alike. Blackrock CEO and Chairman Larry Fink boldly stated: “It is my belief that the next 1,000 unicorns won’t be a search engine, won’t be a media company. They’ll be businesses developing green hydrogen, green agriculture, green steel, and green cement”. All tech companies and investors should pay close attention to ensuring good governance and understanding European disclosure requirements (see Articles 8 and 9 in the Sustainable Finance Disclosure Regulation (SFDR)).

We discussed last year the need to put a greater emphasis on diversity and inclusion and sadly not much has improved on that front. In 2021, diverse teams captured only 9% of the capital raised, despite there being clear evidence that they out-perform non-diverse teams. Although Pitchbook posits that talent will remain the biggest challenge for start-ups, we believe that the talent will, should and must come from increasingly diverse pools of candidates.

It is widely thought that while there will still be significant growth into 2022, the growth will likely be slower this year. With the rate of growth expected to plateau slightly, it is posited that the amount of lateral hires made this year will be similar to the amount made in 2021. Diversity is of course an issue for some of the law firm teams as well as we feel that this might have an impact on both lateral hiring and promotions in this space in 2022.

As Europe continues to cement itself as a giant in the world of VC, we will be interested to see how to trends of individual countries develop and compare to the trends that have been occurring in the UK.

The Investment funds market has been overheating throughout 2021, and with good reason. Last year, many investment funds were impacted by the economic issues and general instability created by Covid-19; many assets were quickly sold and there were substantial capital outflows from funds in a “dash-for-cash” which affected financial markets globally.

Economic recovery has been steady, and the deployment of capital has sped up as sponsors are coming back with the plan to raise larger and more diverse funds to be able to resiliently combat any further unrest within the financial markets. This is evidenced by the growing relevance of secondary funds, which is a way to refinance an existing fund and manage the risk while improving the liquidity of the asset. This alongside increasing GP led transactions, restructurings, NAV financings and single asset deals has meant the market has been very busy for lawyers! It seems the secondaries market is still growing and the pipeline seems healthy with diversification on everyone’s mind. Kirkland & Ellis hiring secondaries expert Társis Gonçalves in July 2020, a senior associate from Paul Hastings, highlights that they obviously believe it will continue to grow and have backed emerging talent.

The Investment Association reported in their annual survey that, despite economic and social upheaval, both assets under management (AUM) and funds under management (FUM) for UK members had grown by 11%, reaching £9.4 trillion and £1.4 trillion, respectively, by the end of 2020. The UK continues to host the largest investment management centre within Europe, and the second largest globally.

Data from the IA’s survey has shown that 49% of the £9.4 trillion AUM incorporated environmental, social, or governance (ESG) factors into the investment processes, a significant increase from 37% in 2019. In this same vein, FUM in Responsible Investments (RI) grew by 60% throughout 2020 – the percentage of UK investor FUM in RI remains small but is steadily growing, reaching 3.9% from 2.6%. Other trends identified within the industry were increased investments in technology, catalysed by remote working, and an overall trend towards promoting diversity and inclusion within firms. This could be seen with Silver Lake amassing $20bn for the largest-ever tech-focused buyout fund which will target global large-cap technology firms.

We thought with such a busy LP and GP market it was worth taking a closer look at the lateral hiring trends that have been taking place over the last 3 years:

2021

Name

Leaving

Joining

Kate Troup

Charles Russel Speechlys

Fladgate

Barry Stimpson

Womble Bond Dickinson

Shoosmiths

Ted Craig

Dentons

Paul Hastings

Edyta Brozyniak

MJ Hudson

Charles Russell Speechlys

Rosalyn Breedy

Wedlake Bell

Simons Miurhead & Burton

Jonathan Powling

Addleshaw Goddard

DLA Piper

Winston Penhall

Reed Smith

Keystone Law

Steven Ward

Paul Hastings

Squire Patton Boggs

Dale Gabbert

Simmons & Simmons

Fieldfisher

Nick Rainsford

Ashurst

Baker McKenzie

Jeremy Cross

Cadwalader

Addleshaw Goddard

Geoffrey Bailhache

Blackstone

Simpson Thacher & Barlett

Emily Brown

Schulte

Ropes & Gray

Paul Ellison

Macfarlanes

Clifford Chance

Owen Lysak

Clifford Chance

Simpson Thacher & Barlett

James Board

Kirkland & Ellis

Simpson Thatcher

Daniel Greenaway

Mishcon de Reya

K&L Gates

Sophy Lewin

Herbert Smith Freehills

Kirkland & Ellis

2020

Name

Leaving

Joining

Saloni Joshi

MJ Hudson

Alston & Bird

Shervin Shameli

MJ Hudson

Reed Smith

David Selden

Fried Frank

PwC

James Alexander Davison

Addleshaw Goddard

DLA Piper

Oliver Rochman

Morrison & Foerster

Morgan Lewis

Robert Mailer

Morrison & Foerster

Morgan Lewis

Tom Alabaster

Linklaters

Ropes & Gray

Justin Cornelius

BCLP

Goodwin

Michael Newell

Norton Rose Fulbright

Cadwalader

2019

Name

Leaving

Joining

Andrew Hougie

Dechert

W Legal

Jonathan Blake

O’Melveny &Myers

Herbert Smith

Warren Allan

Stephenson Harwood

Proskauer

Shaun Lascelles

Vinson & Elkins

Akin Gump

John Daghlian

O’Melveny & Myers

Akin Gump

John McGrath

Sidley Austin

Dechert

Leith Moghli

Reed Smith

Proskauer Rose

Zoe Connor

Haynes & Boone

Addleshaw & Goddard

Nicola Hopkins

Bryan Cave

Ashurst

Andrew Shore

Proskauer

Kirkland & Ellis

Daniel Quinn

O’Melveny & Myers

Akin Gump

Ted Craig

MJ Hudson

Dentons

Thiha Tun

Akin Gump

Dechert

James Tinworth

Stephenson Harwood

Fieldfisher

Jasmine Amaria

Walkers

Carey Olsen

We have identified four main trends within the investment funds lateral market.

Over the last three years, there has been a large number of moves, particularly dominated by the US firms’ increasing appetite. There has been significant movement between US firms, for example, the Morrison & Foerster team moving to Morgan Lewis in 2019 and James Board’s move in March 2021 from Kirkland & Ellis to Simpson Thacher. Moves like this demonstrate the clear desire for growth in the top US firms, however, they have started to cannibalise each other, seemingly only taking from US firms, and hiring very few partners from leading UK firms. If this continues to follow this progression, it may lead to a fall out which could see partners looking to return to a UK firm for a different environment. This has been seen in other practice areas before, and it could very well happen here in the near future. It is important to note that there are significantly fewer UK Partners leaving for US firms in recent years, with the notable exception departures from MJ Hudson.

Kirkland & Ellis is a firm which has grown exponentially in recent years, becoming the largest Investment Funds teams in the City – they have hired over 40 lawyers in the last 12 months to become a 30 Partner, 80 fee earner investment funds team. While they have promoted a handful of associates to partners – 3 in 2021 to be precise – the vast majority of their growth has been through lateral moves including some first-time partners. Goodwin Proctor, who have recently had a ‘hiring spree’, which saw them reaching the same size London Investment Funds team as Simpson Thacher; they have managed to become one of the market leaders in terms of investment levels, however they are still operating on relatively smaller deals overall.

While there are not a huge number of moves from in-house to private practice, they are still a significant identifier of trends within the market. Simpson Thacher has taken two significant hires from in-house in the past few years. Earlier in 2021, Geoffrey Bailhache joined, formerly General Counsel at Blackstone, bringing him back to private practice after nearly a decade in-house. In 2020, they also hired Vandana Harris as a Senior Counsel, who was previously the Managing Director of Investment and Inclusion at Unreasonable Capital.

There has been a high volume of internal promotions across US and UK firms in this area. In the last few years, Kirkland & Ellis have made up 8 partners; Clifford Chance has made up 4; Linklaters promoted 4; and, Debevoise made up 2. Travers Smith is a large team which is completely developed through organic and semi-organic growth, as they conduct almost no lateral hires. However, they have only made up one person from the funds team, Ed Ford, into the partnership this year.

There is also continued and potentially increasing congestion within the investment funds market. Ropes & Gray have redeveloped their offering this year by hiring Tom Alabaster, formerly at Linklaters, and Emily Brown from Schulte. Squire Patton Boggs were also able to kickstart their practice by bringing in Stephen Ward, formerly a Senior Associate at Paul Hastings, another firm backing junior talent.

It is clear that firms have a desire to cash in on all the activity that is happening with investment funds. While a decade ago, it was perceived that the best method of getting funds work was through M&A and transactions, there is a clear sense now that the way in is to do funds work, and then progress to transactions. The real question is if all this activity will potentially lead to a boiling point and then some fall out?

Written by Gwen Shaw & Syed Nasser

Syed Nasser, Head of Technology Transactions & Venture Capital

Legal work in Data Protection & Privacy has experienced steady growth over the past decade, across the world, as the storage of people’s information, interactions and tendencies has become a regulated and developing market.

Fides Search recently delivered a talent mapping project for a global financial institution who had instructed us to build their legal data protection function. This exercise highlighted that a vast number of lawyers had, over the last 5 years, been promoted to the partnership at their firm or moved to senior in-house roles (click here for link to post).

Considering this, I have reviewed the movement of law firm Partners that practice within the field of Data Protection / Cyber Security, within the London market.

The Market

The need for law firms to offer data protection advice is now well established. The following statistics demonstrate the importance of offering data protection expertise as it is relevant to law firm clients in any number of sectors:

88 per cent of UK data breaches are caused by human error.

Every 14 seconds a business will fall victim to a ransomware attack. In 2021 it is predicted to be 11 seconds!

Even the least effective training programmes have a 7-fold ROI

71 per cent of customers say they would take their business elsewhere after a data breach

ICO fines can be a huge expense and require massive resource allocation.

In recent years, the UK government has taken significant steps to position the UK as a world leader in data driven innovation. Data has of course played a key part in tracking and tackling the pandemic, further demonstrating how data crosses and touches almost all sectors, whether it be tracking our contacts or tracking our habits for our next food delivery. What this all means is that the UK has a healthy regulatory framework and combined with a government that is very much in favour of having high standards when it comes to data and utilising it to the maximum effectiveness to drive commerce.

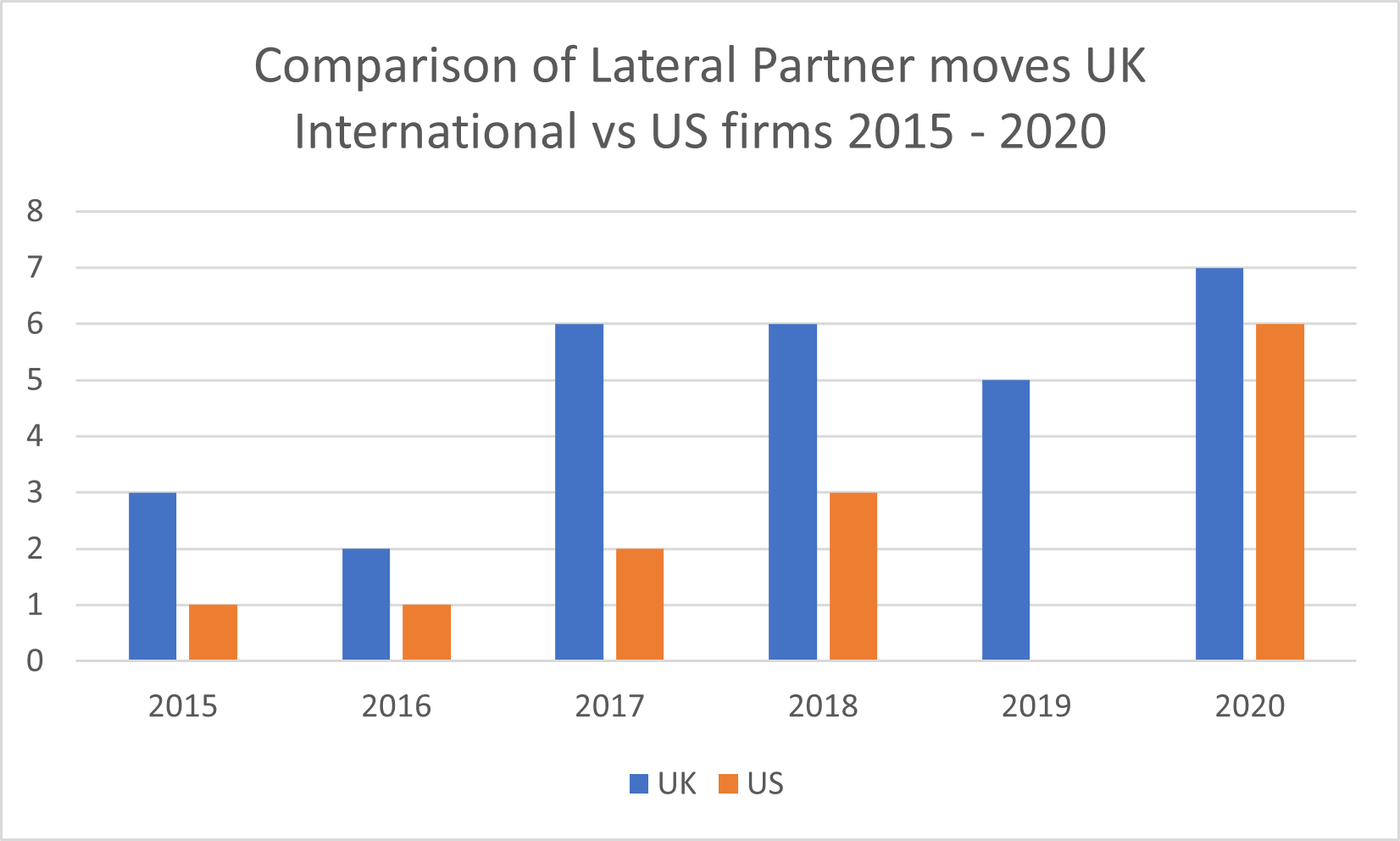

Whilst 2018 was a bumper year for the practice in terms of work levels with GDPR implementation, the ripple in the industry had in fact started the year prior, before which, during both 2015 and 2016, only 4&3 lateral partner moves occurred respectively. In 2017, 8 moves took place with UK/International firms making up 75% of the moves compared to 25% from US Headquartered firms.

This information was gathered via LinkedIn research, moves monitoring sites and law firm announcements.

The trends are clearly linked to regulatory change. 2020 saw several interesting regulatory challenges arise, the Schrems 2 ruling and also the formation of a post Brexit regulation landscape, all stimulating increased work levels and leading to the demand of lateral hires at firms looking to add this practice or add bench strength to their offerings.

It is also important to consider the link with cyber security, and how mass adoption of cloud and web based technologies during the pandemic, whether it be food delivery or establishing the worldwide phenomenon of working from home. We have greatly increased our use of the internet and therefore shared more of our data and the increase in the number of moves in 2020 reflects this.

The US market for data protection is of course somewhat different and evolving quickly as each State has their own data protection regulations and guidelines which create more opportunities when it comes to offering advisory and transactional support which the chart below illustrates as a comparison of UK International firms to US firms.

UK/International firms are responsible for the majority of the lateral moves in London, which is understandable due to the number of firms and an interesting barometer of where the market has been most active from 2015 to 2020 inclusive. Below you can see a year-by-year breakdown:

Below is a list of the partner moves, broken down by year, who offer data protection / cybersecurity in their practice:

2021

Acquiring Firm

Partner

Hired From

Mischon De Reya

Ashely Winton

MWE

Harcus Parker

Ryan Dunleavey

Stewarts

Cooley’s

Guadalupe Sampedro

Bird & Bird

2020

Acquiring Firm

Partner

Hired From

DWF

Stewart Room

PWC

BCLP

Geraldine Scali

Sidley Austin

Pinsent Masons

Jonathan Kirsop

Stephenson Harwood

DWF

James Drury-Smith

PWC

Spencer West

Mark Gleeson

Knights PLC

Baker Mckenzie

Paul Glass

Taylor Wessing

Clifford Chance

Simon Persoff

DLA Piper

Orrick

Faraaz Samadi

Millbank

Orrick

Keilly Blair

PWC

Orrick

James Lloyd

PWC

Norton Rose Fullbright

Paul Joseph

RPC

Addleshaw Goddard

Dr. Nathalie Moreno

Lewis Silken

Clyde & Co

Ian Birdsey

Pinsent Masons

2019

Acquiring Firm

Partner

Hired From

Kemp / Deloitte

Marta Dunphy-Moriel

Fieldfisher

TLT

Gareth Oldale

Sharpe Pritchard

Rosenblatt

Anthony Lee

DMH Stallard

Bevan Britten

James Cassidy

Moorfields (Inhouse)

DWF

JP Buckley

Shoosmiths

2018

Acquiring Firm

Partner

Hired From

Bristows LLP

Marc Dautlich

PM

Ashfords

Sarah Williamson

Boyes Turner

Fox & Partners

Ivor Adair

Slater & Gordon

Eversheds Sutherland

Simon Morrissey

Lewis Silken

Irwin Mitchell

Winston Green

Sainsbury’s Bank

Harbottle & Lewis

Sacha Wilson

Bristows

Paul Hastings

Sarah Pearce

Cooley

Reed Smith

Howard Womersley Smith

Taylor Vintners

Hogan Lovells International

Nicola Fulford

Kemp Little / Deloitte

2017

Acquiring Firm

Partner

Hired From

Bristows LLP

Robert Bond

Charles Russell Speechly’s

Farrer & Co

Ian De Freitas

BCLP

BCLP

Kate Brimstead

Reed Smith

MWE

Ashley Winton

White & Case

Charles Russell Speechlys LLP

Jonathan McDonald

Travers Smith

Reynolds Porter Chamberlain

Jon Bartley

Pennington Manches

Bird & Bird

Guadalupe Samepedro

Paypal

Kemp little / Deloitte

Anita Bapat

Hunton

2016

Acquiring Firm

Partner

Hired From

Rose Fulbright

Lara White

RPC

DLA Piper

Ross Mckean

Olswang

Allen & Overy

David Smith

ICO

2015

Acquiring Firm

Partner

Hired From

Bird & Bird LLP

James Mullock

Osborne clarke

White & Case LLP

Tim Hickman

Hunton

Wedlake Bell

James Castro-Edwards

PWC

Baker & Mckenzie

Dyann Heward-Mills

GE Capital

Diversity and Inclusion

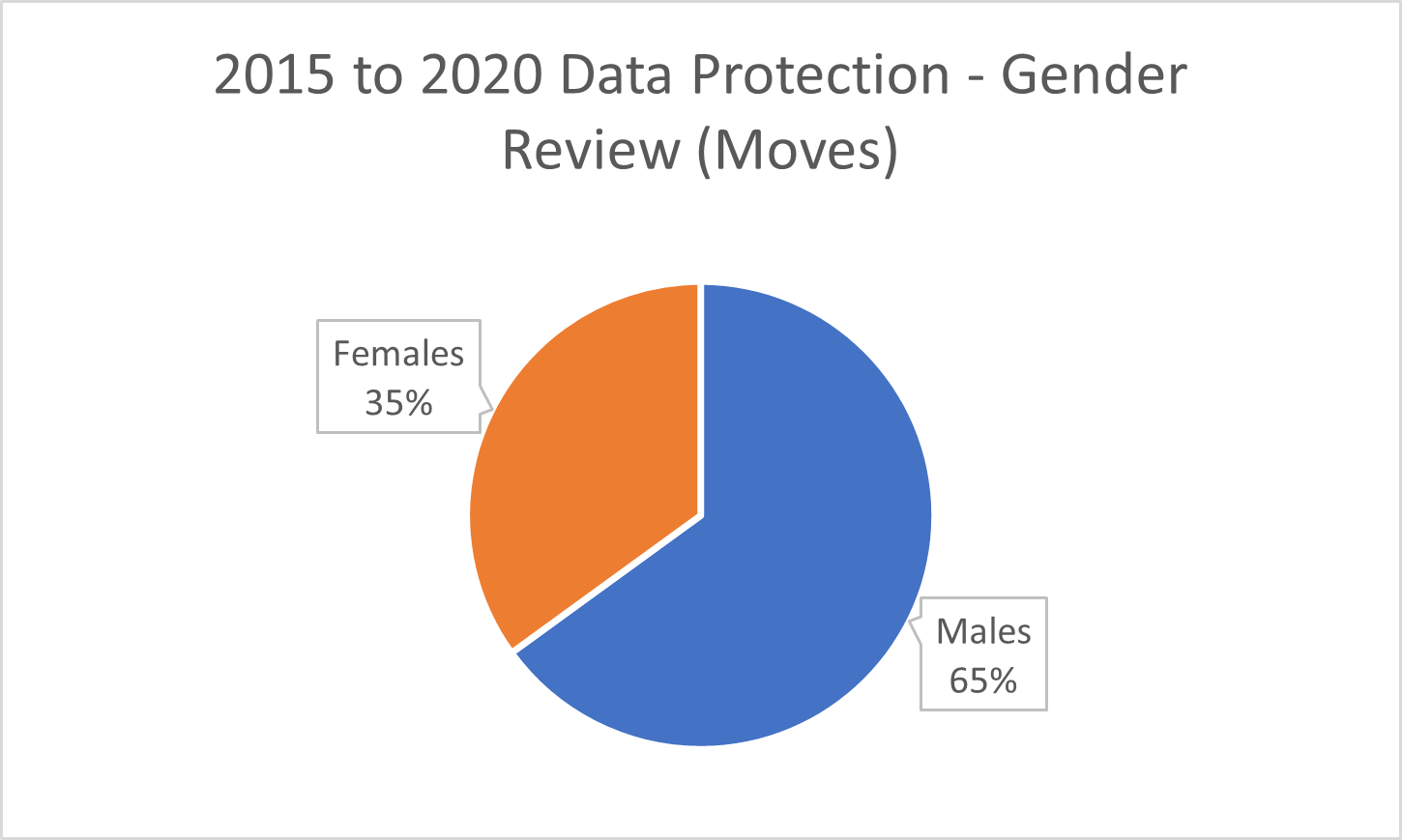

Below see the comparison between Male v Female partners on a year by year basis.

According to the SRA, women make up 50% of firms with 50 plus partners, which is higher than the 47% of the UK women workforce. However, the problem becomes apparent when we look at seniority statistics as women partners make up only 29% of firms with 50 plus partners. What is positive to see from the below chart is that the moves in the data protection space show 35% are female Partners, which shows that whilst there is a way to go it is the correct side of the 30% line.

Internally we have revamped our internal D&I policy to better promote the equality of women and ethnic minorities. While this will increase equality, the benefits of diversity and inclusion are well documented:

“For every 10 per cent improvement in gender diversity, you’d see a 2-4 per cent increase in profits.”

“Diversity means more debate and more perspectives and so better decisions,”

“That leads to better business practices, more innovation, and improved risk taking.”

A think tank found that 48 per cent of companies in the US with more diversity at senior management level improved their market share the previous year, while only 33 per cent companies with less diverse management reported similar growth.

Data protection as a practice area continues to be stimulated by regulatory change and commercial pressures. Schrems 1, Schrems 2 and Brexit are all playing a role in increasing the need for advice, transactions, and dispute resolution within data protection.

The trend clearly indicates the demand for data protection lawyers increased in the run up to 2018. Following which less activity less activity in US law firms resulted in a tailing off in 2019. There is now a clear upswing in demand. 2020 highlighted that the market is growing again and that US international firms are acquiring significant practitioners. This will continue to grow as class actions become more frequent, lets face it the breaches are not slowing down and there will be increased opportunities to litigate.

Law firms may look to add to their transactional and disputes offering. 2021 is off to a quick start with all signs pointing to a similar if not a higher number of partner moved. It is likely that US firms will be a key driver of market moves as US data protection and cyber security practices will aim to connect London with their European practices.

Mathew is a Consultant at Fides Search. He dedicates his time to working with clients on their key strategic hires within TMT and the Data Protection & Cyber security market. To find out more get in touch with Mathew:

In London, new research from Dealroom.co and London & Partners revealed that 2020 was a record year, with tech firms raising $10.5bn of VC investment. London has been the second fastest-growing global tech hub since 2016, seeing increasing levels of new VC funds set up, and being home to the highest concentration of unicorns and future unicorns in Europe. Whilst once Private Equity was the darling of the City when it came to law firm hiring, VC is stepping up to the plate with an increasing number of our law firm clients talking to us about their desire to either establish or add strength to their VC teams.

Why has this happened? Simply put, VC has potential to provide better returns and be more profitable on a public market equivalence basis. Not to mention of course that the lines between PE and VC continue to blur with PE having to adopt the VC model, better understand technology companies, take more risks and drive growth through diversification. Fundamentally, technology has bridged the gap between PE and VC and the trend is set to continue and probably will accelerate after the Covid-19 pandemic recedes, according to Private Equity News.

So let us turn our attention to what this means in the world of lateral partner recruitment at law firms in London, first by taking a look at some of the key Partner moves over the last 5 years:

2020

Acquiring Firm

Partner

Hired from

Latham & Watkins

Shing Lo

Bird & Bird

Latham & Watkins

Mike Turner

Taylor Wessing

Reed Smith

Sam Webster

Mayer Brown

Brown Rudnick

Neil Foster

Baker Botts

Brown Rudnick

Tim Davison

Baker Botts

Brown Rudnick

Sarah Melaney

Baker Botts

2019

Acquiring Firm

Partner

Hired from

Goodwin Procter

Ali Ramadan

Orrick, Herrington & Sutcliffe

Goodwin Procter

Adrian Rainey

Taylor Wessing

Goodwin Procter

David Mardle

Taylor Wessing

Goodwin Procter

Rob Young*

Taylor Wessing

Goodwin Procter

Andrew Davis

Taylor Wessing

Osborne Clarke

Matthew Edwards**

Inventages

Wilson Sonsini Goodrich & Rosati

Stacey Kim

Orrick, Herrington & Sutcliffe

Shoosmiths

James Klein

Pennington Manches

* Rob Young is a tax partner specialising in venture capital transactions

**Matthew Edwards joined from an in-house position at a VC fund manager

2018

Acquiring Firm

Partner

Hired from

Goodwin Procter

Sophie McGrath

Brown Rudnick

Bird & Bird

James Baillieu

Norton Rose

WithersTech

James Shaw

JAG Shaw Baker

WithersTech

Tina Baker

JAG Shaw Baker

WithersTech

Erika McIntyre

JAG Shaw Baker

WithersTech

Susanna Stansfield

JAG Shaw Baker

WithersTech

Ian Cockburn

JAG Shaw Baker

Orrick, Herrington & Sutcliffe

Ali Ramadan

Bird & Bird

Note – Withers acquired JAG Shaw Baker, a corporate and Intellectual Property boutique, to create WithersTech

2017

Acquiring Firm

Partner

Hired from

Shoosmiths

Steve Barnett

Orrick, Herrington & Sutcliffe

Browne Jacobsen

Jon Snade

Irwin Mitchell

2016

Acquiring Firm

Partner

Hired from

Orrick, Herrington & Sutcliffe

Ylan Steiner

King & Wood Mallesons

Taylor Wessing

Angus Miln

Bird & Bird

EY Law

Richard Goold

Gowlings WLG

Ashfords

Giles Hawkins

Orrick, Herrington & Sutcliffe

As we can see, there are some clear trends. In general, the amount of lateral hiring of VC Partners has increased steadily since 2016. Another trend which is more clearly seen in 2020 and 2019, is that major US law firms are hiring Partners in this space. Last year Latham and Watkins established a VC practice, hiring Shing Lo and Mike Turner from UK firms. Brown Rudnick also hired three partners from Baker Botts.

In 2019, Goodwin Procter built a sizeable team including taking four partners from UK firm Taylor Wessing. And 2018 saw the much-anticipated arrival of the leading US tech firm, Wilson Sonsini Goodrich & Rosati in London.

Across the board (with the exception of China, where investment into private technology companies slowed) the size of the market in terms of capital invested into tech, much of it from VCs, has grown steadily, as can be seen below:

In addition, the leading seed investors are raising larger and larger funds and the arrival of leading US VCs means they are now also participating at seed level in Europe. Sequoia Capital opening an office in London is a clear demonstration of this, and Peter Theil recently spoke about why he is increasingly investing into European tech, having previously dismissed it.

It is therefore no surprise that with growing fundraisings and increased investments that law firms are increasing the size of their VC practices and competing for the best talent. Nor is it a surprise, with increasing US VC presence in Europe alongside increased US activity by UK-based start-ups seeking growth, that US law firms are now extremely interested in this area.

It would be no surprise if 2021 was yet another record breaking one bearing in mind there was of course an initial Covid-19 slowdown in Q2 in 2020, with capital flow and investments grinding to a halt before bouncing back so strongly in Q3. Eileen Burbidge, partner at London VC firm Passion Capital, recently stated (Reuters) that she has been ‘seeing pitches back to pre-COVID levels or higher’. Lateral moves have already started with Erika McIntrye joining Taylor Vinters from WithersTech in January 2021.

However, whilst the future is looking bright indeed, there are likely to be some challenges. There has been a growing trend to focus on Diversity & Inclusion within the VC and technology world, which seems to have a greater disparity than one might naturally assume. This is something that we shall investigate further in a follow-up piece, so keep a look out. In the meantime, it would be great to hear from you: what trends are you seeing in the VC and start-up world? Please feel free to get in touch!

By Syed Nasser, Head of Technology Transactions & Venture Capital

Having recently posted on the EUIPO and UPC we now

turn our attention to analyze and assess lateral moves across the intellectual

property market in London. I was also curious to see whether an article I wrote

two years accurately predicted the rise of the full-service IP firm.

It has been no secret that patent attorney firms have

been making a conscious effort to attract more private practice talent over the

past few years. Arguably, this strategy was most successful back in 2014 with

Carpmaels & Ransford taking Ian Kirby from Arnold & Porter, which at

the time was a game changer across the intellectual property world and proved

that moving to an attorney firm actually works and can be a real benefit to

existing clients. This created a domino effect that we are still enjoying.

Digging deeper, lets discuss some key trends, notably

in London; the common theme is that most hires by private practice law firms

peaked in 2016 and 2020. Please find below a snapshot of hires over the last

4-year period. It is interesting to note that not only did seven of these hires

happen by July 2020, which is the most hires in any year since 2016, nearly a

third of all hires were made by US law firms.

You may have noticed from the selection above,

arguably the biggest game changer was Kirkland & Ellis with what was at the

time, a very unexpected announcement to build out their IP capability,

especially as Allen and Overy hired the team from Simmons & Simmons and

were making all the right noises about building their IP capabilities.

There is one move which could be seen as the first real response to attorney firms taking talent from private practice. This is the team move made by Osborne Clarke from Rouse (highlighted in bold)

Now let us see hires made by patent / trademark attorney firms, these hires include, but are not limited to:

Aside from the relatively barren years of 2017 &

2018, we have seen a significant increase in patent experts making the jump

from private practice to patent / trademark attorney firms. We will talk about

some of the reasons behind this in a future article, however it is the most

notable trend we have seen in the Intellectual Property world.

Another trend worth noting is attorney firms hiring

sole practitioners. The IP market is rife with individuals who have decided to

start up on their own and operate under a consultancy banner. For whatever

reason, these sole practitioners have been tempted back into attorney firms. It

is interesting to note that they rarely move to a private practice law firm.

A sole practitioner will already have their own

clients and obviously, no restrictions to work with these clients when they

move, so surely this would be a no brainer for a private practice law firm?

Yes, there is the integration point to consider and perhaps a loss in personal

autonomy however this type of hire would be relatively risk free. It is

somewhat surprising we have not seen too many moves of this nature. Perhaps the

pricing differential between a consultant and law firm partner is too great!

Yes, Covid-19 has had an impact on recruitment plans

for law firms, however, arguably IP is one area that is actually thriving

during this global pandemic, especially across industries such as life

sciences, pharmaceutical, biotech and of course, medical devices. It is

business as usual as far as the IP world concerned.

Additionally, and slightly off topic as this article

is focusing purely on hires within London, we have seen a rise in both private

practice law firms and attorney firms adding to their bench strength in Germany

and The Netherlands. We will speak about this when we look at European market

trends, but it is interesting to note.

So, as you can see from the above, the attorney firms

have been very active taking talent from competitors and beyond over the last

few years. There are no signs that this will slow down, even during Covid-19

and because of the strategic hires attorney firms have made, they are well

positioned to win and take work (and additional talent) from more established

private practice offerings and become a true one stop shop for intellectual

property matters, which was the prediction I made in my article from 2018.

It would be great to hear from you, do you think that

attorney firms have been more successful than private practice law firms in

hiring IP talent? Will this strategy start to tail off over the next couple of

years? Will private practice firms retaliate? What trends have you seen? Please

free to leave thoughts / comments below.

For the purpose

of this article, we will focus purely on patent / trademark attorney and

private practice hires. There will be a follow up discussion focusing on

in-house moves in the intellectual property world. If you would like to receive

further details of all the IP moves over the last 4 years, please feel free to

get in touch: research@fidessearch.com

Newsletter

We use cookies on our website to give you the most relevant experience by remembering your preferences and repeat visits. By clicking “Accept All”, you consent to the use of ALL the cookies. However, you may visit "Cookie Settings" to provide a controlled consent.

This website uses cookies to improve your experience while you navigate through the website. Out of these, the cookies that are categorized as necessary are stored on your browser as they are essential for the working of basic functionalities of the website. We also use third-party cookies that help us analyze and understand how you use this website. These cookies will be stored in your browser only with your consent. You also have the option to opt-out of these cookies. But opting out of some of these cookies may affect your browsing experience.

Necessary cookies are absolutely essential for the website to function properly. These cookies ensure basic functionalities and security features of the website, anonymously.

Cookie

Duration

Description

cookielawinfo-checkbox-analytics

11 months

This cookie is set by GDPR Cookie Consent plugin. The cookie is used to store the user consent for the cookies in the category "Analytics".

cookielawinfo-checkbox-functional

11 months

The cookie is set by GDPR cookie consent to record the user consent for the cookies in the category "Functional".

cookielawinfo-checkbox-necessary

11 months

This cookie is set by GDPR Cookie Consent plugin. The cookies is used to store the user consent for the cookies in the category "Necessary".

cookielawinfo-checkbox-others

11 months

This cookie is set by GDPR Cookie Consent plugin. The cookie is used to store the user consent for the cookies in the category "Other.

cookielawinfo-checkbox-performance

11 months

This cookie is set by GDPR Cookie Consent plugin. The cookie is used to store the user consent for the cookies in the category "Performance".

viewed_cookie_policy

11 months

The cookie is set by the GDPR Cookie Consent plugin and is used to store whether or not user has consented to the use of cookies. It does not store any personal data.

Functional cookies help to perform certain functionalities like sharing the content of the website on social media platforms, collect feedbacks, and other third-party features.

Performance cookies are used to understand and analyze the key performance indexes of the website which helps in delivering a better user experience for the visitors.

Analytical cookies are used to understand how visitors interact with the website. These cookies help provide information on metrics the number of visitors, bounce rate, traffic source, etc.

Advertisement cookies are used to provide visitors with relevant ads and marketing campaigns. These cookies track visitors across websites and collect information to provide customized ads.

Throughout 2022, with both specific in-depth analysis of practice areas such as Data Protection, Venture Capital and Investment Funds, and weekly updates on partner moves, we charted a year full of developments in the legal market. This data collection allowed us to inspect certain individual or clusters of moves and reveal particular trends. On a broader level, this analysis will provide insight on the direction the market is moving; and on a micro level, it reveals the opportunities for strategic hiring. In a turbulent time of change – whether that be the swelling of in-demand NQ salaries, or the difficulties presented by the war in Ukraine – it is even more important that we understand the legal market that we work in.

Throughout 2022, with both specific in-depth analysis of practice areas such as Data Protection, Venture Capital and Investment Funds, and weekly updates on partner moves, we charted a year full of developments in the legal market. This data collection allowed us to inspect certain individual or clusters of moves and reveal particular trends. On a broader level, this analysis will provide insight on the direction the market is moving; and on a micro level, it reveals the opportunities for strategic hiring. In a turbulent time of change – whether that be the swelling of in-demand NQ salaries, or the difficulties presented by the war in Ukraine – it is even more important that we understand the legal market that we work in.

{kind=link}