In a vocation as rigorous and demanding as the legal profession, lawyers with non-visible disabilities have felt the need to cover up the true extent of their impairments, or to hide the fact that they are disabled altogether, out of fear that their employment prospects and career progression will be negatively impacted.

In March 2020, The Solicitors Regulation Authority conducted a study which found that just 3% of solicitors declared they had a disability, a figure which has remained stagnant over the past 10 years. This is in sharp contrast to the 13% of the workforce in the UK who have declared a disability, however through the lens of the Equality Act 2010, which uses a broader definition, this figure is estimated to be around 19%. Non-visible disabilities can include Autism, ADHD, Dyslexia, visual and hearing impairments, and health conditions such as auto-immune disorders and Diabetes.

The study commissioned by the Disability Research on Independent Living and Learning (DRILL) and conducted by Cardiff Business School titled “Legally Disabled? – Career experiences of disabled people in the legal profession” was released. The study drew on focus groups, 55 interviews and approximately 300 survey responses from solicitors, barristers, paralegals, and trainees, where 70% exclusively reported having non-visible impairments and 20% reported having both visible and non-visible impairments. This survey found that of those questioned, 60% of solicitors and paralegals had experienced some form of ill-treatment or bullying at their place of work, and 80% of them believed it was a direct result of their disability. With barristers, 45% of them reported experiencing the same, and 71% believed it was a result of their disability. Over 80% of both groups reported that “poor attitudes/lack of understanding towards am impairment or health condition” was the most significant form of ill-treatment.

Of those surveyed who were disabled when they began their careers, only 8.5% of solicitors and paralegals and one barrister felt confident enough to disclose their impairment when they initially applied. 86% of solicitors and paralegals who have requested adjustments or support reported that doing so “created stress and anxiety for them”.

The implication of these statistics is that there are solicitors and barristers who should have been receiving reasonable adjustments to accommodate their impairments, but they are not asking for them. This could be due to a lack of confidence in their employers to adequately provide these accommodations, or out of fear of creating negative attitudes surrounding their ability, which might impact their careers overall. Either way, the stigma around asking for reasonable adjustments remains a massive barrier in allowing those with disabilities in law to preform to the best of their ability on a daily basis. Even when these lawyers felt confident enough to broach the subject of reasonable adjustments with their superiors, the negative emotions that were consistently associated with the experience do not inspire the confidence needed to continue to be self-advocates, and to champion the need for inclusivity across the spectrum.

Overall, 71% of barristers and 56% of solicitors, paralegals, and trainees felt that they did not have the same potential for career progression as their non-disabled colleagues. The SRA’s study found that there was an overwhelming feeling that their disabilities ‘lowered the bar’ and was “perceived as reducing the standard of competence”. Even in a seemingly inclusive working environment, disabled solicitors and barristers can still be subject to unconscious biases, which can take the form of “rituals, practices, and attitudes that exclude or undermine them”; even if there is no overt intention of discrimination.

It is clear that only “radical positive intervention” can begin to cope with the “uneven playing field” that disabled lawyers are dealing with on a daily basis. There have been a number of recent strides towards promoting inclusive accommodation. Many firms have begun to develop their own Neurodiversity Networks within the firms; these networks can range from focus groups which work on tackling diversity issues, intranet systems which provide educational information on different visible and non-visible disabilities, as well as detailing the accommodations that can be requested and utilised within the firm. These networks have also allowed lawyers who are not neurodivergent themselves but might have neurodivergent or otherwise impaired family or friends receive additional information or support where needed.

Perhaps the most radical recent change is the initiative called ‘Project Rise’, developed by the Law Society’s Lawyers with Disabilities Division (LDD) as a direct result of the “Legally Disabled?” study, aims to promote part-time training opportunities for candidates who might benefit from them. Both Osborne Clarke and Eversheds Sutherland have committed to offering all trainees the ability to work on a part-time basis from September 2024, although both firms currently employ some part-time training candidates.

There is no “one size fits all” solution when it comes to reasonable adjustments and accommodating different impairments; where a part-time training opportunity might help one person, it is not guaranteed to have the same positive results for another. Firms must continue to promote environments which encourage lawyers to come forward where they need adjustments made to help them realize their full potential. In September, the Law Society released a guidance on reasonable adjustments, which detailed the different ways that firms could offer their disabled employees more support. Some of the suggestion include: a ‘passport’ which would detail the needs of that specific employee; continuing to promote flexible work arrangements; physical changes to the offices such as sound-proofed rooms or more suitable furniture; disability equality/awareness training, and; making appropriate changed to billable hours where appropriate.

The legal profession as a whole has been promoting Diversity & Inclusion (D&I) initiatives across the board, seeing an upswing in racial, gender, and socioeconomic diversity in firms nationally and internationally. However, disabled people are often invisible in these D&I programmes, which has only intensified the issues that they face day-to-day and is a major barrier in creating a truly inclusive and open work environment for everyone.

UK Disability History Month aims to celebrate the lives of all people with visible and non-visible disabilities, challenge disablism, and achieve equality.

The Investment funds market has been overheating throughout 2021, and with good reason. Last year, many investment funds were impacted by the economic issues and general instability created by Covid-19; many assets were quickly sold and there were substantial capital outflows from funds in a “dash-for-cash” which affected financial markets globally.

Economic recovery has been steady, and the deployment of capital has sped up as sponsors are coming back with the plan to raise larger and more diverse funds to be able to resiliently combat any further unrest within the financial markets. This is evidenced by the growing relevance of secondary funds, which is a way to refinance an existing fund and manage the risk while improving the liquidity of the asset. This alongside increasing GP led transactions, restructurings, NAV financings and single asset deals has meant the market has been very busy for lawyers! It seems the secondaries market is still growing and the pipeline seems healthy with diversification on everyone’s mind. Kirkland & Ellis hiring secondaries expert Társis Gonçalves in July 2020, a senior associate from Paul Hastings, highlights that they obviously believe it will continue to grow and have backed emerging talent.

The Investment Association reported in their annual survey that, despite economic and social upheaval, both assets under management (AUM) and funds under management (FUM) for UK members had grown by 11%, reaching £9.4 trillion and £1.4 trillion, respectively, by the end of 2020. The UK continues to host the largest investment management centre within Europe, and the second largest globally.

Data from the IA’s survey has shown that 49% of the £9.4 trillion AUM incorporated environmental, social, or governance (ESG) factors into the investment processes, a significant increase from 37% in 2019. In this same vein, FUM in Responsible Investments (RI) grew by 60% throughout 2020 – the percentage of UK investor FUM in RI remains small but is steadily growing, reaching 3.9% from 2.6%. Other trends identified within the industry were increased investments in technology, catalysed by remote working, and an overall trend towards promoting diversity and inclusion within firms. This could be seen with Silver Lake amassing $20bn for the largest-ever tech-focused buyout fund which will target global large-cap technology firms.

We thought with such a busy LP and GP market it was worth taking a closer look at the lateral hiring trends that have been taking place over the last 3 years:

2021

Name

Leaving

Joining

Kate Troup

Charles Russel Speechlys

Fladgate

Barry Stimpson

Womble Bond Dickinson

Shoosmiths

Ted Craig

Dentons

Paul Hastings

Edyta Brozyniak

MJ Hudson

Charles Russell Speechlys

Rosalyn Breedy

Wedlake Bell

Simons Miurhead & Burton

Jonathan Powling

Addleshaw Goddard

DLA Piper

Winston Penhall

Reed Smith

Keystone Law

Steven Ward

Paul Hastings

Squire Patton Boggs

Dale Gabbert

Simmons & Simmons

Fieldfisher

Nick Rainsford

Ashurst

Baker McKenzie

Jeremy Cross

Cadwalader

Addleshaw Goddard

Geoffrey Bailhache

Blackstone

Simpson Thacher & Barlett

Emily Brown

Schulte

Ropes & Gray

Paul Ellison

Macfarlanes

Clifford Chance

Owen Lysak

Clifford Chance

Simpson Thacher & Barlett

James Board

Kirkland & Ellis

Simpson Thatcher

Daniel Greenaway

Mishcon de Reya

K&L Gates

Sophy Lewin

Herbert Smith Freehills

Kirkland & Ellis

2020

Name

Leaving

Joining

Saloni Joshi

MJ Hudson

Alston & Bird

Shervin Shameli

MJ Hudson

Reed Smith

David Selden

Fried Frank

PwC

James Alexander Davison

Addleshaw Goddard

DLA Piper

Oliver Rochman

Morrison & Foerster

Morgan Lewis

Robert Mailer

Morrison & Foerster

Morgan Lewis

Tom Alabaster

Linklaters

Ropes & Gray

Justin Cornelius

BCLP

Goodwin

Michael Newell

Norton Rose Fulbright

Cadwalader

2019

Name

Leaving

Joining

Andrew Hougie

Dechert

W Legal

Jonathan Blake

O’Melveny &Myers

Herbert Smith

Warren Allan

Stephenson Harwood

Proskauer

Shaun Lascelles

Vinson & Elkins

Akin Gump

John Daghlian

O’Melveny & Myers

Akin Gump

John McGrath

Sidley Austin

Dechert

Leith Moghli

Reed Smith

Proskauer Rose

Zoe Connor

Haynes & Boone

Addleshaw & Goddard

Nicola Hopkins

Bryan Cave

Ashurst

Andrew Shore

Proskauer

Kirkland & Ellis

Daniel Quinn

O’Melveny & Myers

Akin Gump

Ted Craig

MJ Hudson

Dentons

Thiha Tun

Akin Gump

Dechert

James Tinworth

Stephenson Harwood

Fieldfisher

Jasmine Amaria

Walkers

Carey Olsen

We have identified four main trends within the investment funds lateral market.

Over the last three years, there has been a large number of moves, particularly dominated by the US firms’ increasing appetite. There has been significant movement between US firms, for example, the Morrison & Foerster team moving to Morgan Lewis in 2019 and James Board’s move in March 2021 from Kirkland & Ellis to Simpson Thacher. Moves like this demonstrate the clear desire for growth in the top US firms, however, they have started to cannibalise each other, seemingly only taking from US firms, and hiring very few partners from leading UK firms. If this continues to follow this progression, it may lead to a fall out which could see partners looking to return to a UK firm for a different environment. This has been seen in other practice areas before, and it could very well happen here in the near future. It is important to note that there are significantly fewer UK Partners leaving for US firms in recent years, with the notable exception departures from MJ Hudson.

Kirkland & Ellis is a firm which has grown exponentially in recent years, becoming the largest Investment Funds teams in the City – they have hired over 40 lawyers in the last 12 months to become a 30 Partner, 80 fee earner investment funds team. While they have promoted a handful of associates to partners – 3 in 2021 to be precise – the vast majority of their growth has been through lateral moves including some first-time partners. Goodwin Proctor, who have recently had a ‘hiring spree’, which saw them reaching the same size London Investment Funds team as Simpson Thacher; they have managed to become one of the market leaders in terms of investment levels, however they are still operating on relatively smaller deals overall.

While there are not a huge number of moves from in-house to private practice, they are still a significant identifier of trends within the market. Simpson Thacher has taken two significant hires from in-house in the past few years. Earlier in 2021, Geoffrey Bailhache joined, formerly General Counsel at Blackstone, bringing him back to private practice after nearly a decade in-house. In 2020, they also hired Vandana Harris as a Senior Counsel, who was previously the Managing Director of Investment and Inclusion at Unreasonable Capital.

There has been a high volume of internal promotions across US and UK firms in this area. In the last few years, Kirkland & Ellis have made up 8 partners; Clifford Chance has made up 4; Linklaters promoted 4; and, Debevoise made up 2. Travers Smith is a large team which is completely developed through organic and semi-organic growth, as they conduct almost no lateral hires. However, they have only made up one person from the funds team, Ed Ford, into the partnership this year.

There is also continued and potentially increasing congestion within the investment funds market. Ropes & Gray have redeveloped their offering this year by hiring Tom Alabaster, formerly at Linklaters, and Emily Brown from Schulte. Squire Patton Boggs were also able to kickstart their practice by bringing in Stephen Ward, formerly a Senior Associate at Paul Hastings, another firm backing junior talent.

It is clear that firms have a desire to cash in on all the activity that is happening with investment funds. While a decade ago, it was perceived that the best method of getting funds work was through M&A and transactions, there is a clear sense now that the way in is to do funds work, and then progress to transactions. The real question is if all this activity will potentially lead to a boiling point and then some fall out?

Written by Gwen Shaw & Syed Nasser

Syed Nasser, Head of Technology Transactions & Venture Capital

A number of the largest banks in Britain have joined investors, insurers, and over 40 countries in making a pledge to phase out the world-wide dependency on coal, the single largest contributor to climate change, at Cop26 this past week, in what might be a last-ditch effort to limit global warming to 1.5 oC.

A coalition of many state and non-state actors have either signed on to the Global Coal to Clean Power Transition Statement or joined the Powering Past Coal Alliance (PPCA). The signatories of the Statement have agreed to accelerate the technologies and policies needed to successfully transition away from coal power to sustainable clean power in the 2030s or as soon as possible thereafter for major economies, with the overall goal of being globally independent from coal power by the 2040s, or as soon as possible thereafter. The PPCA, which was established in 2017, gained 28 new members, raising the total membership to 165 countries, cities, regions, and businesses.

The 33 banks and other financial institutions, including HSBC, Lloyds Banking Group, and NatWest Group who are all members of the PPCA, will play a crucial role in helping achieve independence from coal, as they have all pledged to ending all domestic and international thermal coal financing by 2030 as well as limiting their own individual carbon footprints.

This announcement has had a mixed reception as it does not take in to account other forms of fossil fuel financing. Between 2016 and 2020, sixty of the largest banks invested $3.8 trillion into fossil fuel companies, raising questions about how much money will be committed to the oil and gas industries in the future. Promises that have been made in the past have been scrutinized as current policies and pledges to creating more sustainable business and investments are seen has having too much discretion and “wiggle room”. Ex-Unilever head Paul Polman has spoken out saying that “People are starting to realize that implementing the Sustainable Development Goals — which cost $3 to $5 trillion a year — is significantly less than dealing with these horrendous consequences of inaction. And the financial market is actually the first one to understand that”. The ability to follow through on moving the funds that currently finance coal into more sustainable energy sources, rather than just alternative fossil fuels such as oil and gas will play a key role in the success of these pledges.

With banks taking this next step in the fight against global warming, it is becoming clear that other global business leaders need to take a transformative approach to preserving and protecting the environment through collective action. Inevitably, the outcomes of these agreements will affect the way that law firms and solicitors conduct business on an international scale. Decisions that businesses make will be held under greater scrutiny regarding the impact they have on environmental, social, and governance (ESG) factors, and as these agreements are transitioned into actionable policies and laws, the regulatory landscape will be transformed.

Many law firms have taken individual steps to reduce their carbon footprint, with the likes of Stephenson Harwood launching a scheme that allows employees the ability to lease an electric car through the firm, and CMS planting 8,000 trees after tracking their employee’s carbon footprints.

Browne Jacobson in particular has taken a number of steps to reduce their carbon footprint and have achieved a carbon neutral status within the last year. Beyond creating programmes for sustainable waste management and the recycling of industrial waste produce, such as ink cartridges, as well as financing the CIKEL Brazilian Amazon REDD APD Project, which will use sustainable logging practices to save over 27,000 hectares of rainforest from deforestation, they have begun to incorporate sustainable thinking into their everyday business practices. Projects that are being undertaken within the firm must analyse the amount of carbon output that this is likely to produce, this applies to the entire supply-chain within the firm, including projects with outsider companies. As a firm, they have also been looking into green financing initiatives and advancing clean start – ups to further encourage a more sustainable business practice. Acknowledging an individual’s environmental impact, and thinking diligently about how to offset that, seems to be a practice that is encouraged across the firm as a whole. Browne Jacobson have also been instrumental in showing and giving their support to the “Midlands Engine” which is an established centre of excellence for energy research and innovation- investing now in a broad range of alternative energy technologies that will accelerate energy innovation and the growth of clean energy. They are working in partnership and again, is a great example of how a law firm is going above and beyond to play an integral part in the long term sustainability of the environment.

While individual initiatives show that firms are taking accountability for their carbon output and are committing to more sustainable business practices, the importance of collective action in response to global warming cannot be overstated. As highlighted by the efforts of Cop26, a collective commitment to developing a dedicated approach to reducing and eventually phasing out large scale investment into finite, fossil fuel-based energy sources must be undertaken immediately with substantial investment being funnelled into the implementation of widespread ‘greener’ energy sources including nuclear, geothermal, wind, hydroelectric, tidal and solar systems in order for global businesses to operate in sustainable and environmentally-cognisant ways. Moving forward what can the legal industry do to make the promises and agreements actionable and enforceable?

For more information about Cop26 please contact Gwen Shaw gwen@fidessearch.com

Fides Search are delighted to have participated in the joint venture of Spencer West and Kashwani Law. Spencer West is a leading independent law firm model which offers clients a high level of service led by partners. Kashwani Law are a very well respected law firm based in the UAE servicing a mix of domestic and international clients.

Fides Search have been supporting Spencer West with their international growth. Having considered a number of different entry points into the UAE market, which is key to Spencer Wests Global strategy, it became apparent that a combination with an existing and established player would deliver the best results. Spencer West and Kashwani law have embarked on an exciting and complimentary Joint Venture which will enable them to capitalise on a raft of synergies and complimentary practice groups and sector alignments.

Antoine West, Managing Partner, Spencer West had this to say– “As a growing firm we are continually seeking opportunities to enhance our international presence, Mathew and the team at Fides had been instrumental in advising us on how we could approach this and really took the time to understand our strategy and we were able to find a local partner that matched our ambitions and guide us through the process to a successful conclusion.”

Hassan Kashwani, Partner, Kashwani Law Firm – We have been an established law firm in the UAE market for over 30 years and we have had aspirations to grow internationally as well as growing our offering here, the aspirations of Spencer West and their vision aligned well and from the introduction through to successful completion, Mathew and the team at Fides supported at each stage of the process. – Great!

Jazmine Bernard, Business Development Manager, Kashwani Law Firm – Fides provided us with a clear and consultative introduction to Spencer West and were able to navigate the cultural understanding of doing business in the middle east effortlessly and in turn resulted in a seamless process. The updates and follow ups throughout the process from Mathew were second to none and we are very appreciative of his hard work in this joint venture, we look forward to growing our firm, partnerships and being able to assist our clients not only locally but globally due to the outcome of Mathews introduction and hard work.

Mathew Parker, consultant at Fides Search had this to say, “We knew that Spencer West had international plans and the UAE is a developed legal market as well as a gateway to Asia and Africa. We took a consultative approach to this project and presented suitable options for Spencer West and tailored our approach to optimise their entry into the market. We were excited by the team at Kashwani Law Firm and found them seeking to become more international and bolster their presence locally”

Ed Parker, Director at Fides Search had this to say – Spencer West and Kashwani Law have complete what looks to be a transformative Joint Venture. The spirit of this agreement is underpinned by two motivated law firms seeking to offer multijurisdictional legal coverage to domestic and international clients. Both leadership teams have ambitious plans for the Joint Venture and it is truly exciting to have supported in this endeavour.

It was a real pleasure working with both leadership teams and we wish them all the very best in this endeavour.

September 2021 is now upon us and as many of us prepare for a return to the physical office, there is an overwhelming feeling that things are not as they once were. Numerous city law firms and companies are expecting staff to be in the physical office and although we have all long anticipated a return to the office, it is not yet clear what the impact will be.

The next few weeks will offer a look into the future, we will have a front row seat to a tussle between policy, productivity, tradition, technology and diversity.

What should we expect? Firstly, with very few exceptions the return to the office is talked about in almost every discussion that we have with our clients in the UK. It is best described as a lively discussion and at the very least it is a management headache! Key sectors such as professional services, financial services and technology have transitioned, almost seamlessly, for an extended period of time, into remote working. Most conversations with candidates and clients feature some dialogue around the working dynamic and we have all become accustomed to discussing our specific circumstances and often voicing our preferences. Some might say that we have been able to enjoy bespoke working arrangements. By that we mean if you wanted to work from the physical office it was possible, if you wanted to work from home, well that was the norm and those seeking a balance between the two have actually been able to achieve that. The need to be in the physical office dissipated as a new digital form of collaboration amongst colleagues was enabled through technology rather than office space. For anyone that has visited their physical office however it is clear that uptake has been low, numbers quoted to us have indicated a range of 10-30% but our surveys suggest fewer than 10 % have actually been traveling into the office regularly.

We conducted three surveys during the height of the pandemic. We sought to understand the impact that the pandemic was having on working dynamics. Why three surveys? At the time we genuinely thought that there would be a start, a middle and an end to the pandemic. The reality however was not as we first anticipated. Survey 1 was conducted at what we thought was ‘early pandemic’ which was 2 – 4 weeks after the first lockdown in the UK commenced. Survey 2 was what we felt was the midpoint, this was at 6-8 weeks. As we sought to complete the final survey we realised that a return to normal was not within sight. So we paused, choosing to complete the picture as we advanced towards what was eventually dubbed ‘freedom day’. But even with ‘freedom day’ looming the return to the office did not crystalise. There are a number of contributing factors towards this, not least rising levels of infection widely reported in the news. Employers in sectors such as professional services, financial services and technology have instead largely focused on September, or the end of the summer, for the watershed moment.

Why it has taken so long to return to the office is of course debatable but for argument sake it is worth first acknowledging just how well the legal industry has performed in the remote working environment. Every aspect of day to day business that could be performed remotely, has been performed remotely and there have been some surprises along the way. This is not to say that parts of our economy haven’t been hard hit however.

What are challenges employers might face? 45.2 % of respondents would prefer to work from home post the restrictions.

What was a temporary shift has turned into a long term way of working. With almost half of the sampled respondents ‘preferring’ to work from home post restrictions lifting; employers take note. This result shows a shift in attitude when it comes to working from home. Employers seeking to get the most out of their talented employees must now reflect on a staggering shift in perception. 23.3% of respondents indicated that they didn’t mind working from home, only 26% responded that they prefer to work in the office. With only 4 % responding that they are unsure. This is a clear thumbs up to remote working.

Let’s now look at the fear factor. 42.5% of those who were concerned about returning to the office listed “the commute to the office” as their primary concern compared to 17.8% who said their main concern was a “safe work environment”

Our survey shows that commuters are more concerned about their journey to work than their safety whilst working in the office. These concerns are due to the lack of infection control, social distancing and health and safety precautions during the commute. Nonetheless, employers are not able to factor the safety of the commute of their employees into their return-to-work strategy as this is beyond their control. Whilst not all respondents work in congested urban environments an overwhelming number do. It is simply not productive to have employees arrive pre or post rush hour, this simply extends congestion times and is disruptive. Whilst there are alternatives to public transport these are not necessarily accessible to all and given that an overwhelming percentage of respondents listed the commute as their primary concern it begs the question, how do employers seek to distil this concern?

What are we expecting from the return to the office? 60 % of respondents said they “would expect to work 2-3 days in the office once restrictions lift.”

As it stands, law firms have differed in their approach to the return-to-work strategy. Some have decided to return to their offices three times a week, others like Allen & Overy are looking to open their premises fully, while some are planning to open at 50% capacity, with desk booking systems and extra cleaning measures in place. Other firms such as Simmons & Simmons are gradually allowing employees to return to the office once a week to meet with their team until the firm’s hybrid policy commences. Several others are taking a more cautious approach and using the summer to explore different working patterns.

Arguably it is too early to settle on a long-term approach to office re-entry or agile working, considering new variants and the constant changes the pandemic brings. Even today we are waiting to see the impact the return to schools will have. Only 15.3% of respondents said that they would expect to work 5 days per week from the office. This represents a staggering shift in mentality.

59% of respondents said their employer has communicated a return to the office strategy.

This is not all together surprising, there is no one size fits all policy, trial and error is likely the way forward. After all what does 50% in office time mean? Is that 2.5 days per week, is that 2 days one week 3 days the next, is it a rough guide, is it an aspirational value or could you spend 6 months in the office and 6 months at home. It means all of the above, potentially! What happens when a team member contracts Covid-19, should teams be split into bubbles or should they seek to be in at the same time in order to collaborate better. Prior to March 2020, leaders had the fortune of a one size fits all approach. Is it irresponsible for the office to re-open whilst some are not vaccinated or further still, should vaccinations become mandatory? As we work through a period of unprecedented change in terms of the office working dynamic, it is clear to see that there are more questions than answers.

What should we look for?

Should employers consider productivity a key barometer? The legal industry offers us a glimpse into what may be a tangible gain from the Covid-19 pandemic. Prior to March 2020 the office environment was considered the only environment to house a large employee base. We now know that there is an alternative, however the alternative thrived as the majority were working from home, we achieved a form of level playing field. Service provider and service seeker both found themselves working from home, leaders and their teams all found themselves working from home, single adults and adults with children all found themselves at home. Not only was it a level playing field but respect crept in, people had to respect each individuals specific situation. Empathy and understanding prevailed.

The pandemic created different and unique challenges for those on their own and for those with young families, those with partners working on the front line and those with partners who lost their livelihoods or were as a result of the pandemic forced to work under challenging conditions. However…the mean productivity rating out of 10 was a 7.6 with most respondents grading their productivity between a 7 and 10 out of ten. This is a phenomenal finding as average would have been a 5. Employees clearly feel like their productivity is enhanced by working from home. Big Law has clearly been party to this productivity gain as most major firms have enhanced both their revenue and profitability during the pandemic.

On top of productivity gains 63% of respondents expressed that their loyalty to their employer had increased and that as a result they were less likely to leave. Only 12.3 % of respondents expressed that they are less loyal and actively considering a new role. For those employers hoping to capitalise on pandemic related hiring opportunities this perhaps provides an insight into the reason unemployment figures have been falling and numerous media outlets have reported on a lack of supply in the labour market.

76% of respondents answered “No” to, “does your employer currently have a hiring freeze in place?” This statistic has changed from 50 % during the height of the pandemic.

While people have enjoyed the benefits and flexibility of working from home, there is a consensus seemingly of an overwhelming need at the junior and trainee level for a return to the office. Is there an optimum level? There is no denying the benefit of learning by osmosis, simply being around experienced individuals creates a learning environment. It also enables real time corrections to take place, which can be a major hurdle in a remote working scenario. Furthermore, we have emerging evidence to support that trainees and junior lawyers have expressed that working from home has had a negative impact on their mental health, their need for more supervision and their desire to develop boundaries between work and home life. During the height of the pandemic 89% of respondents either agreed or strongly agreed that ‘working from home is more productive when a significant percentage of the work force is accustomed to working from home’.

Whatever the office dynamic looks like moving forward, the ‘new normal’ and the transition to a hybrid model will be more challenging than the shift to universal home working. Law firms and companies will have to consider new ways of managing significant numbers of employees who will be split between home and the office. Firms that will succeed are those that communicate effectively and keep the needs of their lawyers and clients at the forefront.

Now we must decide, are we a fist pumper, foot tapper, elbow bumper or hand shaker?

If you haven’t heard of #blockchain then where have you been? Many people shy away from new concepts or think, I’ll figure it out when it concerns me.

Blockchain does concern you. This tech has been operating for years. It is already mainstream and in the not too distant future it will permeate all aspects of society and no longer carry such an alien stigma.

There is so much more to blockchain technology than cryptocurrency. That is an obvious statement, but many people just associate blockchain with bitcoin.

Yes, #Bitcoin operates using blockchain, but what actually is blockchain?

Blockchain is a system of recording information.

It is a system that is immutable, meaning you can’t change the data that’s been recorded.

(Well… a #quantumcomputer may be able to, but that’s a post for another day!)

It is essentially a #digitalledger of transactions that is duplicated and distributed across an entire network of computer systems on a blockchain, which makes near impossible to hack.

You may have come across the acronym #DLT which stands for Distributed Ledger Technology, essentially what is described above. A DLT is a decentralized database managed by multiple participants, across multiple nodes.

The transactions are then grouped in blocks and each new block includes a hash of the previous one, chaining them together, hence why distributed ledgers are often called blockchains.

Are you lost?

Let’s try and simplify: A blockchain is a database shared across a network of computers.

Think of the actual concepts, “block” and “chain”.

The record will detail the transaction, including a digital signature from each party.

Stage Two

The record will be validated by computers in the network.

These computers are called, “nodes”.

Stage Three

The validated records are added to a block.

Each block contains a unique code called a hash.

Stage Four

The block is added to the chain.

The hash codes connect the blocks together in an order.

This creates a #BLOCKCHAIN.

Making sense?

Uses

The bottom line is that this technology offers (for the moment) unrivalled security for the storage of data. Because of this, there are numerous uses. The most recognisable is probably #cryptocurrency, but we can park that immediately given that Blockchain isn’t all about #crypto.

Let’s consider some mainstream uses below:

Financial Institutions

Banks and other financial institutions have been investing in blockchains to streamline their transactions record-keeping. This is probably a need as opposed to a want given that they are at risk if they do not keep up with digital currencies.

Property

It wasn’t all that long ago that we had paper deeds for our houses, bibles of parchment paper that looked as though it had been scribed with a quill. But now 87% of homes in England and Wales are registered. By registered, this means the data is stored on a central database at the UK Land Registry. If these records were stored on a blockchain, this could cut down on costly title research and insurance. It will also help resolve historical issues of ownership.

Products/Retail

Recording trades on a blockchain offers a way to check the history of a product. For example, the luxury fashion brand #LVMH (Louis Vuitton Moet Hennessy), is launching a blockchain to help consumers track the authenticity of their products. AURA has been built using a version of the Ethereum blockchain called #Quorum, which is focused on data privacy and was developed by #JPMorgan. This software should boost consumer confidence if it is able to validate the origination of the product. Particularly in industries, for instance, the diamond industry to assure customers that diamonds are not sourced from places where they could finance war.

Healthcare

Have you ever tried to access your medical records? They are usually stored on a database and you have to submit a request for them. They aren’t easily accessible and there is usually an admin fee for the luxury of obtaining your healthcare data. Using blockchain, could allow medical records to be decentralised, but stored safely and securely, which would allow more accessibility and patient control.

Summary

Whilst only a few have been considered above, there is a huge appetite for the inherent possibilities of blockchain technology.

The global blockchain market size is expected to grow from $1.06 billion in 2020 to $10.45 billion by 2025. This is astronomical growth that some consider on a par with the evolution of the internet and personal computer technology (Report Linker. “Blockchain Services Global Market Report 2021: COVID 19 Growth and Change to 2030.” Accessed May, 2021).

If you don’t know about Blockchain technology, be curious because it is #thefuture.

Glossary of terms

Bitcoin: A type of well known digital currency founded by Satoshi Nakamoto in 2009.

Blockchain: A specific type of database that stores data in blocks that are chained together.

Cryptocurrency: A form of digital asset, usually maintained by a decentralised system.

DLT: aka Distributed Ledger Technology, which is essentially a record of transactions shared across a network of geographical locations, held by nodes, which eliminate the need for a centralised third party. These are considered highly secure due to their immutability.

Ethereum: A decentralised, open-source blockchain with smart contract functionality founded by Vitalik Buterin a Canadian-Russian Programmer.

Hash: A function that meets the encrypted demands needed to solve a blockchain computation. It is the backbone of the blockchain network.

Nodes: Nodes form the infrastructure of blockchain. A node contributes to the network of a blockchain by communicating with other nodes to assess validity.

Quorum: An enterprise blockchain platform being used to support business needs.

Venture Capital (VC) remains all the rage in London and Europe with record levels of investment in 2020 and a clear pattern of increased hiring in the VC space by law firms as we saw in our Transfer Market piece. However, as alluded to at the conclusion of that article, when discussing VC, there is a huge challenge when it comes to Diversity & Inclusion.

Lack of diversity within VCs

According to Forbes in 2019, of the 2,114 venture capital professionals in the U.K, 76% of them are white, compared to the 59% population of London, where most of the funds are located, with women making up 20% of that percentage. These numbers become even worse when you consider the statistics from Diversity VC on the decision makers, which show women make up only 13% of decision-making positions in U.K VC.

Lack of diversity in investments

These figures are incredibly problematic as VC firms help shape the next generation of technology companies by pumping billions of dollars into businesses. The lack of diversity amongst VC decision-makers is reflected in the businesses that typically receive funding from them. According to statistics accumulated by Dealroom.co, of total capital invested in European tech in 2020, 91% went to all-men founder teams whilst just 9% went to teams with at least one woman founder.

Extend Ventures, a Not-For-Profit which aims to diversify access to finance conducted research to see how VC was invested in the U.K between 2009 and 2019 amongst 3,784 entrepreneurs who started 2,002 businesses within that period. The report found that ethnic-minority groups received a total of just 1.7% of the venture capital made at seed, early and late stage over this period.

Atomico meanwhile found that looking at the composition of the founder respondents to the State of European Tech survey based on self-reported ethnicity, 83% of all founders identified as White/Caucasian. Only 2% of all founder respondents self-identified as Black/African/Caribbean, and none of those respondents raised external capital! Mandela Schumacher-Hodge Dixon recently wrote that ‘As a Black woman, I’m part of a demographic that’s least likely to successfully raise venture capital’.

The challenge

But why is that and why are the statistics so bad? It is not, by any means, the only industry to have challenges around D&I and we know only too well here at Fides Search that our law firm clients who support VCs, entrepreneurs and tech companies face their own challenges. We spoke to a few leaders working within the VC/Tech space to gain some insight into the challenges faced by the industry:

Elena Pantazi, Head of Talent and Portfolio Development at Northzone, told us that there are a number of reasons for this such as ‘recruiting from a handful of non-diverse organisations in the first place and relying mainly on warm introductions to build up teams, leading to inherent bias’.

Richard Goold, Head of Tech Law and Fast Growth at EY Law UK, told us that ‘VC is a small industry, and the network is strong – the lack of diversity throughout is therefore somewhat self-perpetuating’.

Yvonne Bajela, Founding Member and Principal of Impact X Capital Partners, said that ‘there is a lot of research out there that highlights the fact that there is systematic and unconscious bias.’

Mike Rebeiro, who is currently Chairman of Adoption UK and previously the Global Head of Technology at Norton Rose Fulbright, believes that ‘most VCs come from City backgrounds, which remains white and male-dominated. They will naturally invest into businesses where they feel some empathy and sympathy, so through conscious or unconscious bias, they will largely invest into businesses founded by people of a similar background and profile.’

He went on to say that ‘law firms and accountancy firms have, in recent years, undertaken a wide variety of training on microaggression and unconscious bias. I have my doubts that this happens in the VC and investment space; they naturally run leaner business models and lack the necessary expertise.’

Elena points out that historically there has been ‘limited understanding of why diversity is important in business and how it ultimately leads to better outcomes.’ But there is now at least a growing consensus that things need to improve because as Mike says, ‘it isn’t just the right thing to do morally speaking, but it fundamentally makes business sense’.

The benefits of a diverse workforce

Inclusive and diverse workforces enable better decision-making, better performance and better results. A study by Gompers & Kovali showed that not only did varied teams make better decisions, but they also made better investments. “The success rate of acquisitions and IPOs was 11.5% higher on investments by partners with diverse school backgrounds, and 22.0% higher for those from ethnically diverse backgrounds”. This is likely to be especially true of innovative technology businesses because as Mike pointed out ‘the best innovation comes from diversity of opinions and the diversity of solutions’.

Companies led by diverse management teams are better equipped to compete in a global economy due to the diversity in opinion. There is a “33% higher likelihood of industry-leading profitability for the companies in the top quartile for ethnic diversity” according to Launch with GS. Richard sums it up nicely pointing out that the evidence clearly shows ‘that diverse teams are stronger and, frankly, better’.

While associating with people from similar backgrounds and cultures may have its benefits, such as providing a sense of shared culture and belonging, it is clear from the evidence presented over the years, particularly in the VC space, that neglecting diversity and inclusion results in a huge financial sacrifice for companies, investors, and firms. Yvonne believes that ‘diversity of thoughts and ideas is just so powerful’ that it can no longer be ignored by those chasing profitability.

Progress on diversity

So there is growing acceptance of the benefits that diversity can bring but how serious is the effort to improve things and how focused are VCs on it both internally and when it comes to investing? Elena is encouraged to have seen progress in the past few years.

Recent data from the BVCA and Level 20 shows that female representation has now risen to 30% in the industry. ‘Nevertheless, it’s fair to say that it is still a long way from being a reflection of society, especially with respect to ethnicity and socioeconomic representation.’

There is no question that progress to date has been slow, so what needs to improve and how? Elena makes the point that ‘we have seen that more diverse teams attract diverse candidates’, and this would be a natural place to start for Venture Capital firms. This will naturally help to change things when it comes to investing but it is, as Richard says, ‘frustratingly slow’ and according to Yvonne ‘despite the fact people are now openly talking about diversity in VC and tech, we are still a long way from cheques being written to rectify this’.

There will be some natural progress as decision-making teams become more diverse, but a more proactive approach is required. Elena told us that at Northzone, there are ‘active and continuous efforts to track the diversity of our deal flow, review our investment process end-to-end and sponsor a number of programmes that enable entrepreneurial talent to flourish. We found that going through the Diversity VC assessment process and achieving certification has been a great way for us to keep ourselves focused and to track the impact of our initiatives’.

Solutions

Our contributors also mentioned a range of other sensible steps that should be taken including, such as education and training on unconscious bias, microaggression and the benefits of D&I both culturally, but also from a business and commercial perspective. Richard told us that the training he and his fellow EY Law partners go through is extensive and that there is no reason investment firms should not be doing the same as professional service firms in this regard.

Diversity targets also have a major role to play. A great recent example seen in the legal industry is that Coca Cola have taken bold strides to make diversity and inclusion a business imperative by announcing to their outside counsel that 30% of billed time must be from diverse attorneys, of which 50% must be black attorneys, or risk having a 30% non-refundable reduction in fees payable.

This can be mirrored in VC by setting targets for women- and multicultural-led businesses in portfolios, as a practical way of improving diversity. An example of this is Goldman Sachs “Launch with GS”, which is a $1 billion investment strategy grounded in its data-driven thesis that diverse teams drive strong returns. Through this strategy, Goldman Sachs aims to increase access to capital and facilitate connections for women, Black, Latinx, and other diverse entrepreneurs and investors.

Role models have an important part to play, and Mike does not believe that there are enough visible female and ethnic minority role models to inspire the next-generation of talent. Ultimately, he feels, ‘to effect serious and long-lasting impactful change, government will have to intervene with legislation as self-regulation and organic progress will never suffice’.

The role of Search Firms

We asked our contributors whether they thought Search Firms had a role to play and Richard was very clear: ‘Yes! Having a D&I mindset and helping to build diverse teams is a critical part to this role’.

Elena believes ‘a search firm that can proactively unearth high quality, diverse talent will undoubtedly be adding differentiated value in the mid to long run’, while Yvonne made the point that she does not ‘believe there is a shortage of pipeline and you need search firms who proactively ‘go outside of the usual circles’ when looking for talent.

Here at Fides, we have, since our inception championed diversity and inclusion, and have revamped our internal policy to reflect this. For example, when mandated on roles, at least 30% of our longlists are female with a minimum of two female candidates on every shortlist. We recently hired an inclusion lead and are also currently working hard internally to develop a manifesto on ethnicity which we hope to be able to share with you shortly…

Article written by :

Syed Nasser, Head of Technology Transactions & Venture Capital

Fides Search are delighted to announce the appointment of Inka Fukalova as Head of Delivery.

Inka has extensive experience running complex and strategic projects for legal and professional services clients throughout Europe and Middle East. She has been involved in numerous high profile lateral partner appointments and team moves across variety of practice areas, such as Real Estate & Construction, Insurance, TMT just to name a few.

Inka believes in an informed consultative approach to search and working in partnership with Clients and Candidates to achieve successful outcomes. Inka will be playing a key role in the development of Fides’ Delivery Team, which will greatly enhance our search and selection process and ensure consistently high standards of delivery. More to follow on this!

Inka spent last 13 years at a leading global search firm where she was Head of Executive Search, she was instrumental in developing their legal search capabilities as well as managing their CRM database and GDPR protocol.

Inka had this to say:

I’m excited to join the team at the time of exponential growth. Fides is a great example of a genuine search firm with a client centric strategy based on nurturing long-term working relationships and acting as a strategic advisor to their clients and candidates. I’m looking forward to being a part of a collegiate team and delivering first class client service.

Ed Parker had this to say:

We have always wanted to be at the cutting edge of innovation, many see innovation as adapting technology based solutions, but innovation can also be the development of new ways of working that improve outcomes for clients. This is exactly why we are so excited to see Inka join the team. She is absolutely the right person for us to grow a new area of the business which is our Delivery team. Not only is Inka a very experienced search professional but she has also developed countless consultants over the years and she has led research teams whilst also been very hands on when it comes to client relationships. This mix of experience is exactly what we needed for the development of the Delivery Team.

If you would like to connect with Inka her contact details are as follows:

Legal work in Data Protection & Privacy has experienced steady growth over the past decade, across the world, as the storage of people’s information, interactions and tendencies has become a regulated and developing market.

Fides Search recently delivered a talent mapping project for a global financial institution who had instructed us to build their legal data protection function. This exercise highlighted that a vast number of lawyers had, over the last 5 years, been promoted to the partnership at their firm or moved to senior in-house roles (click here for link to post).

Considering this, I have reviewed the movement of law firm Partners that practice within the field of Data Protection / Cyber Security, within the London market.

The Market

The need for law firms to offer data protection advice is now well established. The following statistics demonstrate the importance of offering data protection expertise as it is relevant to law firm clients in any number of sectors:

88 per cent of UK data breaches are caused by human error.

Every 14 seconds a business will fall victim to a ransomware attack. In 2021 it is predicted to be 11 seconds!

Even the least effective training programmes have a 7-fold ROI

71 per cent of customers say they would take their business elsewhere after a data breach

ICO fines can be a huge expense and require massive resource allocation.

In recent years, the UK government has taken significant steps to position the UK as a world leader in data driven innovation. Data has of course played a key part in tracking and tackling the pandemic, further demonstrating how data crosses and touches almost all sectors, whether it be tracking our contacts or tracking our habits for our next food delivery. What this all means is that the UK has a healthy regulatory framework and combined with a government that is very much in favour of having high standards when it comes to data and utilising it to the maximum effectiveness to drive commerce.

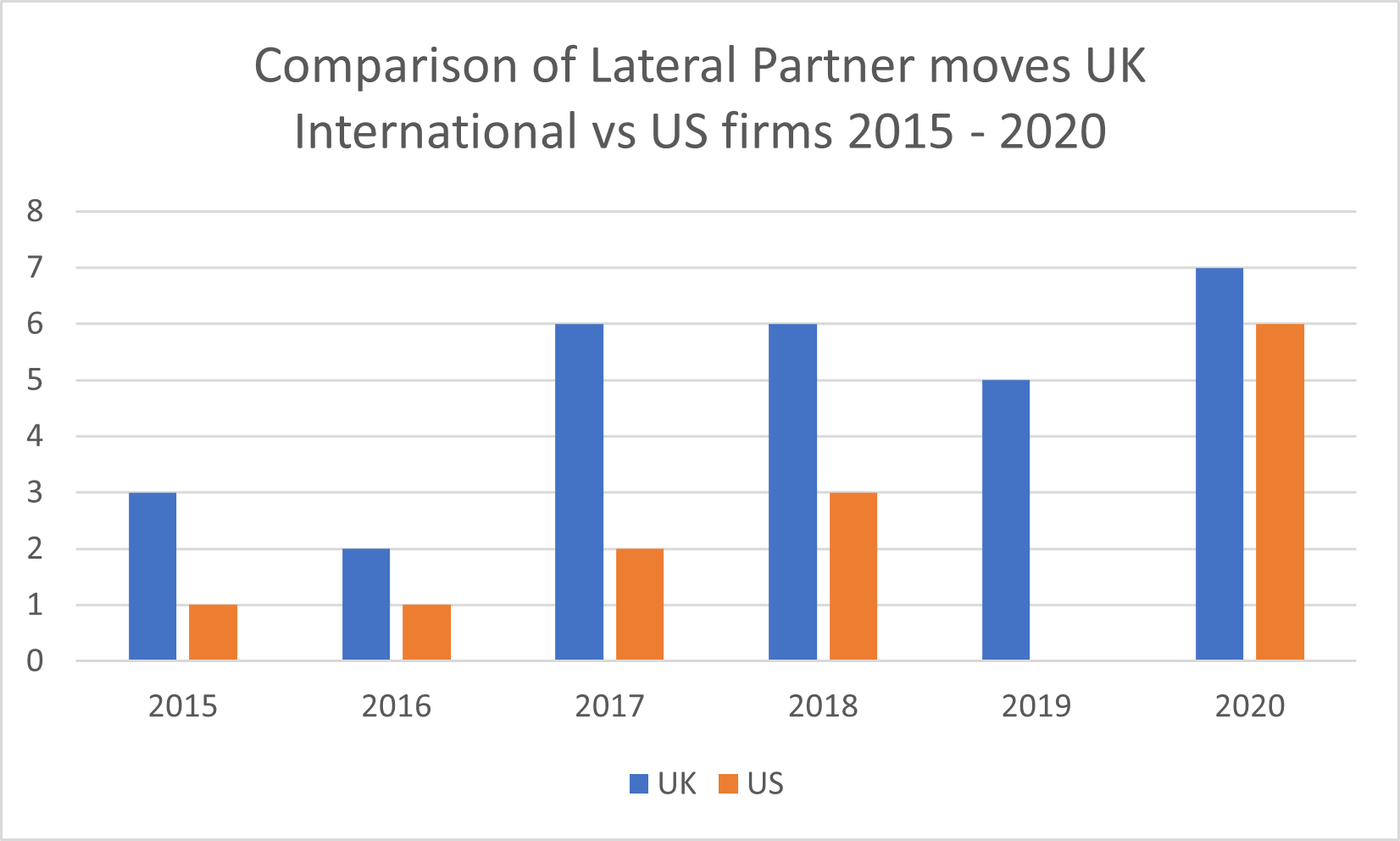

Whilst 2018 was a bumper year for the practice in terms of work levels with GDPR implementation, the ripple in the industry had in fact started the year prior, before which, during both 2015 and 2016, only 4&3 lateral partner moves occurred respectively. In 2017, 8 moves took place with UK/International firms making up 75% of the moves compared to 25% from US Headquartered firms.

This information was gathered via LinkedIn research, moves monitoring sites and law firm announcements.

The trends are clearly linked to regulatory change. 2020 saw several interesting regulatory challenges arise, the Schrems 2 ruling and also the formation of a post Brexit regulation landscape, all stimulating increased work levels and leading to the demand of lateral hires at firms looking to add this practice or add bench strength to their offerings.

It is also important to consider the link with cyber security, and how mass adoption of cloud and web based technologies during the pandemic, whether it be food delivery or establishing the worldwide phenomenon of working from home. We have greatly increased our use of the internet and therefore shared more of our data and the increase in the number of moves in 2020 reflects this.

The US market for data protection is of course somewhat different and evolving quickly as each State has their own data protection regulations and guidelines which create more opportunities when it comes to offering advisory and transactional support which the chart below illustrates as a comparison of UK International firms to US firms.

UK/International firms are responsible for the majority of the lateral moves in London, which is understandable due to the number of firms and an interesting barometer of where the market has been most active from 2015 to 2020 inclusive. Below you can see a year-by-year breakdown:

Below is a list of the partner moves, broken down by year, who offer data protection / cybersecurity in their practice:

2021

Acquiring Firm

Partner

Hired From

Mischon De Reya

Ashely Winton

MWE

Harcus Parker

Ryan Dunleavey

Stewarts

Cooley’s

Guadalupe Sampedro

Bird & Bird

2020

Acquiring Firm

Partner

Hired From

DWF

Stewart Room

PWC

BCLP

Geraldine Scali

Sidley Austin

Pinsent Masons

Jonathan Kirsop

Stephenson Harwood

DWF

James Drury-Smith

PWC

Spencer West

Mark Gleeson

Knights PLC

Baker Mckenzie

Paul Glass

Taylor Wessing

Clifford Chance

Simon Persoff

DLA Piper

Orrick

Faraaz Samadi

Millbank

Orrick

Keilly Blair

PWC

Orrick

James Lloyd

PWC

Norton Rose Fullbright

Paul Joseph

RPC

Addleshaw Goddard

Dr. Nathalie Moreno

Lewis Silken

Clyde & Co

Ian Birdsey

Pinsent Masons

2019

Acquiring Firm

Partner

Hired From

Kemp / Deloitte

Marta Dunphy-Moriel

Fieldfisher

TLT

Gareth Oldale

Sharpe Pritchard

Rosenblatt

Anthony Lee

DMH Stallard

Bevan Britten

James Cassidy

Moorfields (Inhouse)

DWF

JP Buckley

Shoosmiths

2018

Acquiring Firm

Partner

Hired From

Bristows LLP

Marc Dautlich

PM

Ashfords

Sarah Williamson

Boyes Turner

Fox & Partners

Ivor Adair

Slater & Gordon

Eversheds Sutherland

Simon Morrissey

Lewis Silken

Irwin Mitchell

Winston Green

Sainsbury’s Bank

Harbottle & Lewis

Sacha Wilson

Bristows

Paul Hastings

Sarah Pearce

Cooley

Reed Smith

Howard Womersley Smith

Taylor Vintners

Hogan Lovells International

Nicola Fulford

Kemp Little / Deloitte

2017

Acquiring Firm

Partner

Hired From

Bristows LLP

Robert Bond

Charles Russell Speechly’s

Farrer & Co

Ian De Freitas

BCLP

BCLP

Kate Brimstead

Reed Smith

MWE

Ashley Winton

White & Case

Charles Russell Speechlys LLP

Jonathan McDonald

Travers Smith

Reynolds Porter Chamberlain

Jon Bartley

Pennington Manches

Bird & Bird

Guadalupe Samepedro

Paypal

Kemp little / Deloitte

Anita Bapat

Hunton

2016

Acquiring Firm

Partner

Hired From

Rose Fulbright

Lara White

RPC

DLA Piper

Ross Mckean

Olswang

Allen & Overy

David Smith

ICO

2015

Acquiring Firm

Partner

Hired From

Bird & Bird LLP

James Mullock

Osborne clarke

White & Case LLP

Tim Hickman

Hunton

Wedlake Bell

James Castro-Edwards

PWC

Baker & Mckenzie

Dyann Heward-Mills

GE Capital

Diversity and Inclusion

Below see the comparison between Male v Female partners on a year by year basis.

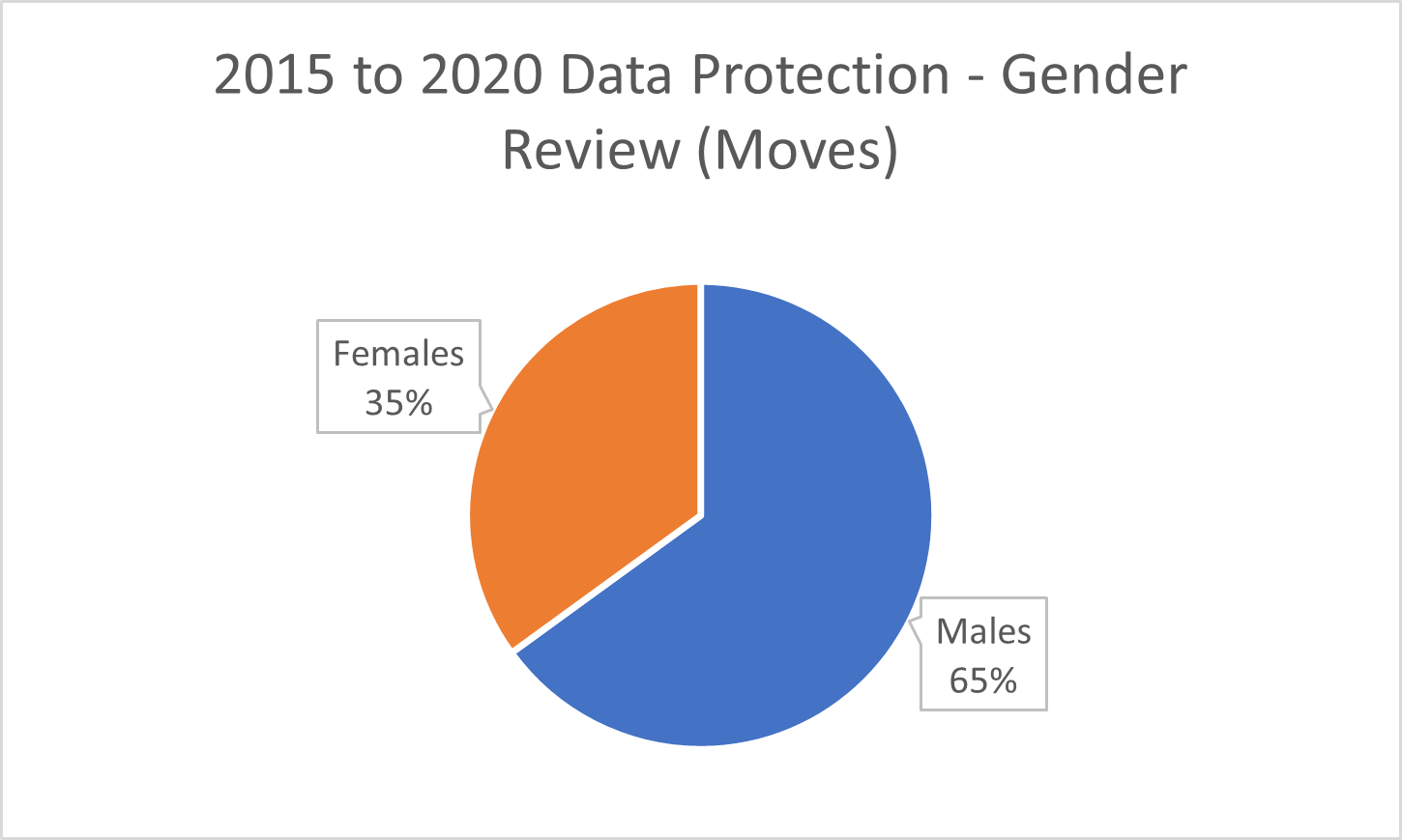

According to the SRA, women make up 50% of firms with 50 plus partners, which is higher than the 47% of the UK women workforce. However, the problem becomes apparent when we look at seniority statistics as women partners make up only 29% of firms with 50 plus partners. What is positive to see from the below chart is that the moves in the data protection space show 35% are female Partners, which shows that whilst there is a way to go it is the correct side of the 30% line.

Internally we have revamped our internal D&I policy to better promote the equality of women and ethnic minorities. While this will increase equality, the benefits of diversity and inclusion are well documented:

“For every 10 per cent improvement in gender diversity, you’d see a 2-4 per cent increase in profits.”

“Diversity means more debate and more perspectives and so better decisions,”

“That leads to better business practices, more innovation, and improved risk taking.”

A think tank found that 48 per cent of companies in the US with more diversity at senior management level improved their market share the previous year, while only 33 per cent companies with less diverse management reported similar growth.

Data protection as a practice area continues to be stimulated by regulatory change and commercial pressures. Schrems 1, Schrems 2 and Brexit are all playing a role in increasing the need for advice, transactions, and dispute resolution within data protection.

The trend clearly indicates the demand for data protection lawyers increased in the run up to 2018. Following which less activity less activity in US law firms resulted in a tailing off in 2019. There is now a clear upswing in demand. 2020 highlighted that the market is growing again and that US international firms are acquiring significant practitioners. This will continue to grow as class actions become more frequent, lets face it the breaches are not slowing down and there will be increased opportunities to litigate.

Law firms may look to add to their transactional and disputes offering. 2021 is off to a quick start with all signs pointing to a similar if not a higher number of partner moved. It is likely that US firms will be a key driver of market moves as US data protection and cyber security practices will aim to connect London with their European practices.

Mathew is a Consultant at Fides Search. He dedicates his time to working with clients on their key strategic hires within TMT and the Data Protection & Cyber security market. To find out more get in touch with Mathew:

Fides Search is delighted to welcome Suzanne Jeffers to the team.

Suzanne joins us as Consultant and will be working on strategic hires for law firms and patent attorney firms as well as in-house appointments across a range of sectors. She will also play a key role in our continued growth in IP & Patents.

Suzanne studied her undergraduate LLB at University of Liverpool and completed her postgraduate LPC at BPP University. She was admitted as a Solicitor of the Senior Courts of England and Wales and practised real estate law prior to taking a leap into legal search & consultancy.

Suzanne has an extremely varied background having worked for both high street firms Foskett Marr Gadsby & Head LLP as well as top 20 law firms Irwin Mitchell and DWF LLP. Her ability to efficiently navigate complex and challenging transactional situations brings praise from clients for her bespoke, responsive and flexible approach. Suzanne adds to our London based capability and will also support our clients in Continental Europe and the Middle East.

She has a passion for legal innovation and regularly attends seminars to discuss the impact of technology in legal services. Suzanne is particularly interested in emerging technologies such as blockchain and crypto assets.

She has a keen eye on cryptocurrencies, their use of blockchain and the reactivity of regulation and compliance. Suzanne thinks it is crucial to uphold the rule of law when it comes to legal tech, but it is also important to strike a balance and avoid stifling progress.

Suzanne joins us at Fides Search during a period of exciting expansion.

Ed Parker, Director had this to say:

‘We are thrilled to welcome Suzanne into the team. She is a truly passionate person and has a deep level of understanding around the legal profession and crucially the future of law. We look forward to introducing her to clients and our network in due course. Suzanne is going to work across a number of areas but crucially is going to support our growth in areas such as IP and Patents.’

Suzanne comment:

‘I’m delighted to be joining Fides! For a number of years prior to qualification as a solicitor I considered a move into legal search consultancy. As cliche as it sounds I love helping people and solving problems – one of the many reasons I got into law! I thrive off client interaction and investigation. I’m excited about this new chapter and very much looking forward to getting to know outstanding people and innovators from diverse backgrounds within the industry!’

Chris comment:

‘I am absolutely thrilled and delighted that Suzanne has joined the intellectual property team here at Fides. Her experience within the law will be an invaluable asset to the wider Fides proposition and I personally look forward to working alongside Suzanne and continue the growth and success of Fides’ intellectual property team.’

Newsletter

We use cookies on our website to give you the most relevant experience by remembering your preferences and repeat visits. By clicking “Accept All”, you consent to the use of ALL the cookies. However, you may visit "Cookie Settings" to provide a controlled consent.

This website uses cookies to improve your experience while you navigate through the website. Out of these, the cookies that are categorized as necessary are stored on your browser as they are essential for the working of basic functionalities of the website. We also use third-party cookies that help us analyze and understand how you use this website. These cookies will be stored in your browser only with your consent. You also have the option to opt-out of these cookies. But opting out of some of these cookies may affect your browsing experience.

Necessary cookies are absolutely essential for the website to function properly. These cookies ensure basic functionalities and security features of the website, anonymously.

Cookie

Duration

Description

cookielawinfo-checkbox-analytics

11 months

This cookie is set by GDPR Cookie Consent plugin. The cookie is used to store the user consent for the cookies in the category "Analytics".

cookielawinfo-checkbox-functional

11 months

The cookie is set by GDPR cookie consent to record the user consent for the cookies in the category "Functional".

cookielawinfo-checkbox-necessary

11 months

This cookie is set by GDPR Cookie Consent plugin. The cookies is used to store the user consent for the cookies in the category "Necessary".

cookielawinfo-checkbox-others

11 months

This cookie is set by GDPR Cookie Consent plugin. The cookie is used to store the user consent for the cookies in the category "Other.

cookielawinfo-checkbox-performance

11 months

This cookie is set by GDPR Cookie Consent plugin. The cookie is used to store the user consent for the cookies in the category "Performance".

viewed_cookie_policy

11 months

The cookie is set by the GDPR Cookie Consent plugin and is used to store whether or not user has consented to the use of cookies. It does not store any personal data.

Functional cookies help to perform certain functionalities like sharing the content of the website on social media platforms, collect feedbacks, and other third-party features.

Performance cookies are used to understand and analyze the key performance indexes of the website which helps in delivering a better user experience for the visitors.

Analytical cookies are used to understand how visitors interact with the website. These cookies help provide information on metrics the number of visitors, bounce rate, traffic source, etc.

Advertisement cookies are used to provide visitors with relevant ads and marketing campaigns. These cookies track visitors across websites and collect information to provide customized ads.

In a vocation as rigorous and demanding as the legal profession, lawyers with non-visible disabilities have felt the need to cover up the true extent of their impairments, or to hide the fact that they are disabled altogether, out of fear that their employment prospects and career progression will be negatively impacted.

In a vocation as rigorous and demanding as the legal profession, lawyers with non-visible disabilities have felt the need to cover up the true extent of their impairments, or to hide the fact that they are disabled altogether, out of fear that their employment prospects and career progression will be negatively impacted.