Welcome back to the Fides Weekly Update. Scroll down to see what news stories our Researchers have been talking about this week in the world of legal and compliance – and don’t forget to take a look the Mover & Shakers of the week!

This week:

1) Relocation, relocation, relocation

Offshoring topped the headlines this week as Dentons, Norton Rose Fulbright and DLA Piper were the latest of a string of firms to announce the relocation of a number of support roles to lost-cost service centres across the globe.

DLA are making the largest relocation, as it announced last Friday that up to 200 jobs will be shifted from their UK business services team to their low-cost centre in Warsaw. Amounting to 18% of UK support staff, offices in Sheffield and Leeds are most likely to bear the brunt in this latest round of consultations, with 85 jobs at risk in the firm’s Yorkshire offices and 47 jobs at risk in London.

Dentons also announced that they planned to open a business services centre in Warsaw this week, with the relocation of 50 roles that represents 12% of Dentons UK-based business staff. Dentons Business Services EMEA plans to have 90-100 staff by the end of the year, and is to be directed by Piotr Macieja who joined from global professional services provider TMF.

On the other hand, Norton Rose Fulbright have selected Manila as the destination for their low-cost service centre, revealing that they are opening in The Philippines in September. Aiming to relocate 170 roles – 5% of the firm’s support office jobs globally – 59 jobs have been put at risk in the UK, which equates to 10% of the firm’s London support staff.

Other UK firms to create back office support centres include Freshfields Bruckhaus Deringer, which opened a support centre in Manchester and is aiming to launch a second in Vancouver; Herbert Smith Freehills and Allen & Overy, which both opened support centres in Belfast; and Linklaters, who also have business support functions in Warsaw.

Motivation for law firms to relocate back-office functions outside of the UK goes beyond simple cost cutting measures to further consider how support for lawyers can be made as effective and efficient as possible. For example, the current consultation underway at DLA Piper is part of a global review that started two years ago with advice from McKinsey & Company as to how the firm could operate more effectively on a global basis.

These latest offshoring announcements indicate that law firms continue to cut costs in attempt to drive future profitability. However, to ensure that the quality of support for lawyers (and clients) remains paramount, law firms should also look to innovate and automate some of their support functions for the future.

2) Legal team shake-up

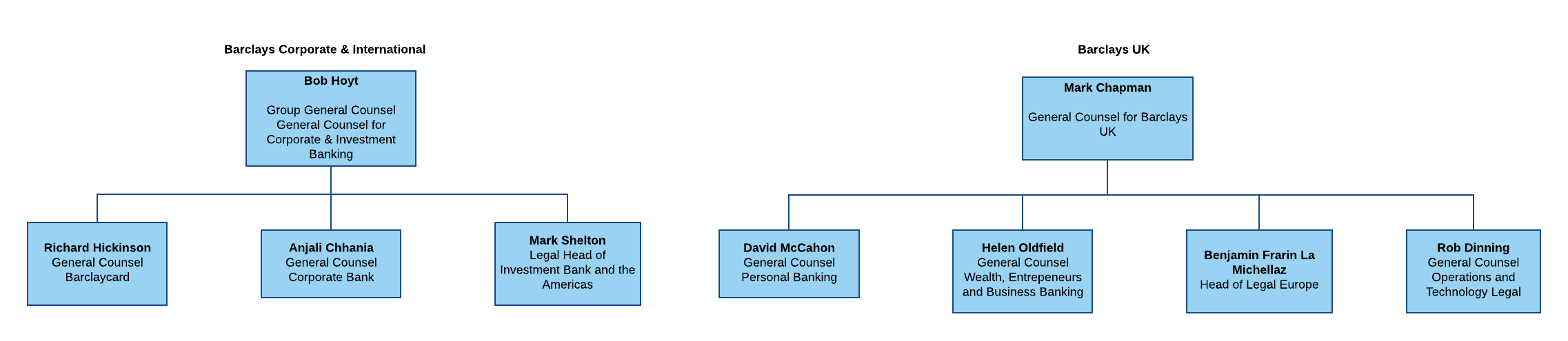

The looming reforms on ring-fencing have brought about a significant restructuring of Barclays’ legal team this week. The bank’s new structure will comprise of two core divisions, Barclays Corporate & International and Barclays UK, with the legal team split to be positioned in either of the two banking arms. On account of the restructuring, senior management for the two legal teams will look as follows:

The Prudential Regulation Authority produced its final policy on implementing ring-fencing regulations in March, which demands all UK banks’ retail arms are separated from the rest of the business and, in particular, away from their investment banking activities. This should in turn protect customers by reducing their exposure to the bank’s high-risk investment banking operations.

Barclays are the first of their competitors to report a legal restructuring on the back of ring-fencing, whilst Lloyds Banking Group made a legal appointment, overseeing their ring-fencing process. Former Berwin Leighton Paisner corporate partner Frances McLeman initially joined Lloyds as their interim head of corporate and M&A legal. She was appointed head of ring-fencing legal in January this year, where she leads their group restructuring plans and banking regulatory reform in relation to ring-fencing.

Whilst Barclays restructure their team to cope with the demands of ring-fencing, Freshfields are also restructuring in an attempt to improve collaboration amongst partners. Individual team practices within the firm’s finance practice will be consolidated to form three larger team practices, which should allow them to better service their clients by providing “more flexibility across the spectrum of debt products”.

Asset, project and aviation finance will form one group, capital markets and corporate treasury will also form another practice and their greenfield, brownfield and bond groups will merge into one infrastructure team.

We plan to see a number of further restructurings taking place, especially within the banking sector as many banks are yet to ring-fence operations. HSBC are expected to implement changes to their retail operations in 2018, which could see a large part of their legal team relocate to Birmingham where the new UK retail and commercial banking head office will be based.

Movers & Shakers of the week

Moves

Lloyd’s of London lose GC

General counsel Sean McGovern has left Lloyd’s of London to join insurance and reinsurance company XL Group as their chief compliance officer, head of regulatory and government affairs

Bird & Bird hire aviation finance expert

Jim Bell has joined Bird & Bird as a partner in their Aviation & Aerospace group in London. He leaves Allen & Overy, where he served as a senior associate in their Structured and Asset Finance group

White & Case add to growing City corporate practice

Hogan Lovells corporate partner Guy Potel has joined White & Case’s corporate practice in London

Proskauer strengthen their real estate offering in London

Joanne Owen, DLA Piper’s former global co-chair of hospitality and leisure, has moved to Proskauer Rose’s London office, where she serve in their real estate practice

Ashurst expand German corporate capability

Former Linklaters corporate partner Holger Ebersberger has joined Ashurst’s partnership and will sit in their Munich office

Pinsents add to Düsseldorf office

Dr. Anke Empting joins Pinsent Masons from KPMG Law in Düsseldorf as a partner to strengthen their energy and life sciences practices

Dentons boost ETI practice

Clyde & Co’s David Moore has moved to Dentons as a partner and will sit in their London Energy, Transport and Infrastructure (ETI) practice.

Office Openings & Closings

Ince & Co set up in Cologne

Ince & Co has hired CMS Hasche Sigle’s head of insurance Stefan Segger, along with two associates to launch their second German office in Cologne. They have also brought on partner Eva-Maria Goergen who joins from local firm Bach Langheid Dallmayr

Norton Rose move back office support to Manila

Norton Rose Fulbright plans to relocate 170 support jobs worldwide, including 60 in London, to a business services centre in Manila

Dentons also choose to set up shared services centre outside the UK

Dentons has announced a new low-cost business support facility in Warsaw, which will lead to the loss of approximately 50 UK roles

Partner Promotions

Travers Smith promotes six to partner

Hello and welcome to the Fides Weekly Update. Take a look at this week’s key trends, moves and developments in legal and compliance.

Tweet us @Fides_Search to let us know your thoughts.

This week:

1) US firms feast on London market

The domination of US firms within the London legal recruitment market was further confirmed this week with the publication of research by Legal Week, which found a 20% increase in lateral partner hires into US firms in 2015.

Last year US-based law firms made 110 lateral partner hires, up from 90 in 2014, making this the highest number of lateral partner hires to be made by this group in the last four years.

With the launch of its first European office in January, Cooley’s was the biggest lateral hire in the London market last year. The firm brought across 24 partners including teams from Edwards Wildman and Morrison and Foerster to open their London office whose headcount now stands at over 60 lawyers.

Other firms that were particularly active in the lateral recruitment market include Morgan Lewis, Ropes & Gray, King & Spalding, Kirkland & Ellis, Morrison & Forrester, Gibson Dunn & Crutcher and White & Case.

However, London expansion was not on the agenda for all US firms with Skadden, Arps, Slate, Meagher & Flom, Sidley Austin and Davis Polk seeing London partner numbers contract over the 12-month period.

In a year that saw high profile hires in the likes of Steve Thierbach to Gibson Dunn, Matthew Elliott to Kirkland & Ellis and David Ereira to Paul Hastings, is the aggressive lateral partner hiring strategy of US firms set to continue?

If the start of 2016 is anything to go by, the trend for US and international firms to boost their London offering looks here to stay.

Last week saw White & Case make a second lateral partner hire from Ashurst as part of their strategy to reach 500 lawyers in the City, and Kirkland & Ellis returning to familiar hunting ground Linklaters for partner hires in tax and private equity.

In April, Cleary Gottlieb Steen & Hamilton made only its third London lateral partner hire in more than a decade with the recruitment of Allen & Overy’s head of non-contentious financial services regulation Bob Penn.

However, the flow of lateral partner hires has been more than just one way with Kirkland losing seven London partners to Freshfields and Sidley’s in February which saw the firm double its notice period for equity partners.

The increase in lateral recruitment trends by US firms from 2015 and beyond show the scale and depth that many US firms have now achieved in the London market.

This will continue to pile pressure on UK firms as they scramble to protect their top talent, with the Magic Circle now looking to compete by reviewing the equity and remuneration structures they have in place to attract high profile partners – as evidenced by Freshfields hiring of Kirkland high-yield partner Ward McKimm.

However the impact of these lateral recruitment trends play out in the future, the one certainty is that for now at least, London is the place to be.

2) Anti-Corruption on top of the agenda

The ‘Panama Papers’ scandal brought about a flurry of protests after it led to the surfacing of multiple cases of corruption, money laundering and tax evasion. As world leaders begin damage control and attempt to deal with the corruption that has now come under the spotlight, the UK has decided to hold an Anti-Corruption Summit, hosted by Prime Minister David Cameron in London, in an attempt to face the global challenges for combating corruption.

Prior to the summit, a UK Country Statement was released, outlining three main objectives: to expose corruption in the UK; to introduce stronger legislation that punishes the corrupt and supports those affected, and to eliminate the culture of corruption.

It seems top executives are all on board with the statement as many have signed a pledge confirming their commitment to collectively crackdown on corruption, particularly in jurisdictions where regulatory frameworks are less developed. The executives involved include a number senior management from law firms, such as Ashurst, White & Case, Allen & Overy, Linklaters and Herbert Smith Freehills.

The firms have released a joint statement in which they profess to “play our part in efforts to prevent the proceeds of crime and corruption from entering legitimate capital and investment markets”.

Whilst law firms are tackling the issue by backing new government policy and regulation, banks are also making steps to improve their stance against anti-money laundering and financial secrecy by culling tens of thousands of existing customers.

The FT reported on Wednesday that Deutsche Bank, Barclays and UBS will be closing between 20,000 and 35,000 customer accounts. These accounts are found within their corporate and investment banking operations and have been deemed “too risky under anti-money laundering rules or…have become uneconomic in light of new regulations”.

The culling has proved worthwhile as plans were announced in the Anti-Corruption Summit that financial services companies are to be made liable for their employees’ complicity in money laundering and fraud. With the onus now on the financial services companies, it is likely we will see a similar overhaul of clients from further institutions.

Professional services firms and financial institutions all seem to be on board with the new measures, and the addition of corporate liability will provide a major incentive for them to improve their financial crime policies and procedures. However, it is difficult to maintain momentum when trying to create systemic change in the financial services industry. We saw similar issues with the FCA’s Senior Manager’s Regime, as it lost its sting when abandoning the “reverse burden of proof” clause, which would have held senior managers to account for compliance failings. Ultimately, time will tell as to whether the fight against corruption will succeed and if it remains a priority on the agendas of the world’s elite.

Movers and Shakers of the week

Appointments

Saudi Aramco appoints new GC ahead of their IPO

Nabeel Al Mansour has been named new general counsel at Saudi Arabia’s state owned oil company Saudi Aramco, after previously serving as deputy general counsel.

Moves

BLP lose head of international arbitration

Kent Phillips has left Berwin Leighton Paisner to join Hogan Lovells in their Singapore office. Jonathan Sacher will replace Phillips as head of international arbitration in London

Sidley enhances London employment practice

Susan Fanning has joined Sidley Austin from DLA Piper and will sit in their labor, employment and immigration practice

Mayer Brown gain energy lawyer in Paris

Olivier Mélédo departs Orrick, Herrington & Sutcliffe to join Mayer Brown in their Banking & Finance practice and Energy group

K&L Gates strengthens energy practice in Milan

Former DLA Piper energy specialist Paolo Zamberletti joins K&L Gates in Milan. He is the fourth addition to the firm’s global energy practice in 2016.

Gowling WLG make double partner hire

Gowling WLG have hired banking and finance partner Matthew Harvey from Dentons and projects partner Andrew Newbery, who previously headed up Herbert Smith Freehills’ Abu Dhabi office, after which he set up his own consultancy in London.

Taylor Wessing bolster their TMC practice

Former Latham & Watkins global technology co-chair Martin Cotterill has made a move to Taylor Wessing, where he will sit in their technology, media and communications practice.

Norton Rose bolster European tax offering

Tax partner Antoine Colonna d’Istria is to join Norton Rose Fulbright from Freshfields Bruckhaus Deringer in Paris

Weil Gotshal gain HSF’s London head of PE

James McArthur, London head of private equity at Herbert Smith Freehills, has joined Weil, Gotshal & Manges in London

Fifth Ashurst partner to join Goodwin Procter in Frankfurt

Ashurst tax partner Heiko Penndorf will join Goodwin Procter’s Frankfurt office after the US firm launched their Frankfurt office with four Ashurst partners

Lathams gain antitrust partner in Germany

Leading antitrust lawyer Michael Esser has joined Latham & Watkins in Düsseldorf as a partner. He previously worked at Freshfields Bruckhaus Deringer’s Cologne office

Office Openings & Closings

DLA plan to axe 200 jobs in UK, focusing on Warsaw centre

DLA Piper consider cutting 200 business support roles in the UK and shifting the roles to their shared services hub in Warsaw.

Ex-CC partner launches boutique in Sydney

Mark Pistilli, former managing partner of Clifford Chance’s office, has set up a corporate boutique in Sydney alongside fellow partner Danny Simmons. The firm will be called Pistilli Simmons.

Dentons launch Munich office

Dentons are setting up their third German office in Munich with the hire of three partners from Norton Rose Fulbright. German head of corporate Alexander von Bergwelt, fellow corporate partner Michael Malterer and tax partner Igsaan Varachia will all be making the move.

Welcome back to the Fides Weekly Update. Here we provide you with the key news, trends and developments in legal and compliance. Scroll down to see the Movers & Shakers of the week.

Follow us @Fides_Search for regular market updates

This week:

1) Battle of the Brands

Wednesday saw the annual release of The Acritas UK Law Firm Brand Index, with Eversheds retaining the top spot for the third year running ahead of DLA Piper and Pinsent Masons.

The most comprehensive annual study of the global legal market, the Sharplegal survey canvasses over 2,400 senior buyers of legal services from across the globe to track how legal buyers select law firms and highlight those law firms winning, and losing, brand equity.

As such, the brand index works as a definitive guide as to which UK legal brands are strongest in the eyes of buyers. Rather than being a reflection of technical competence alone, it reveals which firms are prevalent in the client’s minds, whom they are most attracted to and whom they are most likely to give their work.

Eversheds continues to hold a strong position at the top of the UK brand index, being ranked by legal purchasers as first for mind awareness and favourability. This was particularly the case amongst female clients, with the firm’s ability to offer innovative pricing models having a greater appeal amongst this group. Second-place DLA was this year’s star performer, rising 22 points and 4 ranks on the index from last year and being used most by survey respondents for high value work.

Meanwhile, Slaughter and May came in as the second most improved firm, rising from 7th to 4th place on the brand index and overtaking Magic Circle rivals Clifford Chance (5th), Linklaters (6th) and Freshfields (7th). In fact, Slaughters are the only Magic Circle firm to hold a steady position in the UK market since the survey’s inception, with all other Magic Circle firms loosing brand equity nationally since 2012. Despite this, when the data is split down for London the brand index reveals a very Magic Circle dominated affair, with Clifford Chance ranked top followed by Freshfields and Slaughters.

With the average client working with 20 or more law firms at any given time – and marketed to by many more – the findings of the Acritas brand index are important in understanding what can give law firms a competitive advantage in a market that is fragmented, dynamic and constantly changing.

How the index changes over time is a reflection of which firms are doing a better job of making and maintaining a meaningful impression with clients through experience, relationship development and taking an approach to market that really aligns with clients’ goals and needs.

This year’s results show that firms that honestly assess their practice strengths and align themselves to specific client needs are more likely to be favoured by top UK legal clients. This shows that, like it or not, a cohesive and impressionable brand is an essential strategic tool for UK law firms to maintain their standing in the marketplace.

2) RSA on the Road to Recovery

Quarterly earnings have been coming in hard and fast this week, with HSBC, Shell and SocGen all releasing their financial results. RSA in particular shook up the markets, as their promising results caused a boost in the FTSE 100 Index of 0.3 per cent.

The insurance group beat analysts’ forecasts this year by reporting an operating profit of £548m, up 5 per cent from 2015, and a 2 per cent rise in UK and Irish sales, allowing a solid revenue of £1.57bn for the first quarter of the year.

Such a good start to the year can be attributed to the major internal restructuring, as RSA dispose of a number of overseas businesses, particularly those in Latin America, and reduce their presence from 47 countries down to 12. The company continues to implement it’s cost-cutting programme and has recently completed further sales of its Chile and Argentina businesses.

Concentrating on their most profitable businesses in the UK and Ireland, Canada and Scandinavia is paying off for the insurance company, highlighting their resilience after the abandoned £5.6bn takeover bid with Zurich Insurance last summer. Since then, their share prices are recovering and profits are ahead of expectations.

Chief executive Stephen Hester said RSA’s improvement comes down to changes made on a granular level, by improving their underwriting performance and core business units. He says businesses “have to stop relying on top line growth and instead become more efficient, much as manufacturers did in the 1970s and ’80s.”

Hester also spent £480,000 of his own money in acquiring company shares, a move that demonstrates his confidence in their self-improvement measures and new business model.

Despite rough markets, RSA have delivered encouraging results for the first quarter. However, it will difficult to assess the sustainability of this as cost-cutting cannot be a long-term strategy and insurance markets remain as competitive as ever. Nonetheless, analysts seem hopeful and earnings per share have been tipped to almost triple in 2017.

Movers & Shakers of the Week

Moves

Kirkland hire two further partners from Linklaters

Private equity partner David Holdsworth and tax partner Tim Lowe are the latest partners to join Kirkland & Ellis from Linklaters

General counsel Anja Van Bergen has left Nutreco to join Nomad Foods after the firm acquired €2.6bn company Iglo.

Reed Smith lose senior tech partner

Taylor Wessing has hired former Reed Smith partner Angus Finnegan as new head of the firm’s UK communications group

Lathams boosts competition team in Germany

Competition partner Michael Esser has joined Latham & Watkins’ Düsseldorf office from Freshfields Bruckhaus Deringer in Germany.

W&C hire second Ashurst partner in two weeks

White & Case have hired Ashurst’s London head of disputes Mark Clarke, only two weeks after bringing in former Ashurst equity capital markets partner Jonathan Parry.

HSF hires Bakers’ EMEA head of M&A

Senior corporate partner Sönke Becker joins Herbert Smill Freehills’ corporate team In Düsseldorf, exiting Baker & McKenzie, where his previous roles included chair of the firm’s EMEA M&A practice and prior to that, German corporate practice co-head until 2014

A&O add a three-strong US securities team in Australia

A US securities team from Skadden, Arps, Slate, Meagher & Flom joins Allen & Overy in Australia, after Skadden confirmed it was closing its Sydney offices. Partner Mark Leemen makes the move along with counsel Cécile Baume and associate Matthew Lim.

Osborne Clarke make first lateral hires in over a year

London partner Ashley Hurst is joining Osborne Clarke’s commercial and regulatory disputes team from Olswang, whilst Bristol partner Will Robertson departs Bond Dickinson to join Osborne Clarke’s commercial team, specialising in IT and data protection

Stephenson Harwood launches French real estate practice

Pierre Nicholas-Sanzey has been appointed partner at Stephenson Harwood in Paris to launch a dedicated Paris real estate department. He joins from the Paris office of Herbert Smith Freehills

WFW bolsters corporate offering in Frankfurt

Watson Farley Williams has hired Dr. Christoph Naumann as a partner. He joins from Norton Rose Fulbright where he served as Of Counsel.

Partner Promotions

DAC Beachcroft promotes 12 partners, two in the City

Kennedys promotes seven to partnership

Ashurst add 12 to partnership, 3 in London

Simmons makes up 7 to partner, including 3 in London

DLA Piper makes up 48 partners globally, with 8 in London

CMS makes up 31 partners, including 2 in London

Hello and welcome to the Fides Weekly Update, a breakdown of the week’s key news, moves and developments in legal and compliance.

This month’s blog explores the impact falling oil prices have had on global banks and the outlook this holds for the sector in the future.

Tweet us @Fides_Search to let us know your thoughts and feedback

Featured Blog: Has the broken energy market injured global banks?

As results for Q1 2016 are gradually released by the major global banks and financial institutions, there is one question we are all asking: how much have they been affected by depressed oil prices?

Oil prices have been on a downward spiral, and oil producers and lenders alike are desperately seeking for ways to lift the price… Click here to read further

MOVERS & SHAKERS OF THE WEEK

Moves

Cleary Gottlieb picks up A&O finance regulation head

Allen & Overy’s head of non-contentious financial services regulation Bob Penn joins Cleary Gottlieb Steen & Hamilton.

Barclays Competition Head to join Baker & McKenzie

Baker & McKenzie makes a second high-profile hire from Barclays with MD and Head of Competition Nicola Northway.

Sidley Austin bolsters private equity team with Willkie hire

Leveraged finance partner James Crooks joins Sidley Austin from Willkie Farr & Gallagher

Ashurst capital markets partner to depart for White & Case

Ashurst ECM partner Jonathan Parry makes the move to White & Case

Pinsent Masons picks up former TMT practice head at Simmons

Andrew McMillan, who led the TMT practice at Simmons until 2015 joins Pinsent Masons as a partner within its advanced manufacturing and technology sector (AMT)

Freshfields bolsters US offering with hire of leading Department of Justice white-collar prosecutor

Deputy Chief of the USDoJ’s criminal fraud section Daniel Braun joins Freshfields Bruckhaus Deringer.

Mergers

Reed Smith and Pepper Hamilton call off merger talks

Reed Smith calls off merger talks with Philadelphia-based Pepper Hamilton.

Partner Promotions

Norton Rose Fulbright make up 39 partners globally, with two four in the firm’s London office

CMS promotes 31 to partnership with five in the UK

Eversheds make up 26 partners globally, with four in the firm’s London office

Stephenson Harwood promotes nine to partnership with five in London

Charles Russell Speechlys promotes nine to partnership with six in London

HFW make up 9 partners globally, with three in the firm’s London office

RPC promotes three to partnership in latest round

Irwin Mitchell promotes 13 to partnership with three in London

As results for Q1 2016 are gradually released by the major global banks and financial institutions, there is one question we are all asking: how much have they been affected by depressed oil prices?

Oil prices have been on a downward spiral, and oil producers and lenders alike are desperately seeking for ways to lift the price. Prices set a 2016 high on Thursday at $47.22 a barrel, after having reached twelve year lows in January 2016 at a mere $28 a barrel. The worldwide glut in the oil markets has caused this depression in prices, pushing the cost of crude oil down by 70 per cent since mid-2014. The abnormally high supply coming from the Middle East and a period of serious US production has clashed with the reduction in demand from emerging markets, given their slowdown in economic growth.

Reducing supply and alleviating existing stockpiles is becoming more imperative; however, freezing oil output has proved difficult as we saw from the recent unsuccessful OPEC meeting. The meeting that took place in Doha a couple of weeks ago, in the hopes that all major oil-producing countries would agree to freeze production and thus bolster prices, failed to reach an agreement. It was reported Iran failed to attend the meeting, causing a reluctance for fellow oil-producers to agree on a freeze in their production. The New York Times reported that “Iran had ruled out a production freeze and on the eve of the meeting decided not attend the Doha gathering”.

Even without the production freeze however, there may be hope for a natural decrease in supply. Many argue that such a pickup in production is purely seasonal and down to a US driving period in oil production. The US has been the biggest force behind the drastically high oil output after US shale drillers bombarded the market. Their production hit its peak in April last year at 9.7 million barrels a day and has since been on a gradual decline. The continued decline may encourage fellow oil producers to also decrease output and hopefully rebalance the markets.

Regardless of this outcome, banks with large energy loan portfolios have had to build up reserves to account for the losses they have and will continue to experience from plunging prices. Wells Fargo, Citigroup, Bank of America Merrill Lynch and JP Morgan Chase are the most exposed to the energy sector as they released the most loans during the oil boom, making them more vulnerable to the fall in prices.

Energy financing was perceived as low risk when these loans were first handed out as oil prices were at record highs and showed no sign of abating. Now these banks have billions of dollars’ worth of exposure to the struggling energy industry, particularly because they offset the risk of their energy loans by demanding oil and gas as collateral. This collateral is rapidly losing value and banks have been adding further layers to their capital buffers in an attempt to cushion the losses from these underperforming loans.

Wells Fargo, whose business relies considerably on the mortgage industry, have added a further $200m to its reserves against losses to its loan portfolio. Combining the bank’s total loan portfolio with the $23 billion worth of unfunded commitments to oil and gas companies puts Wells Fargo’s total exposure to the oil and gas sector to an impressive $42 billion. Similarly, Bank of America doubled its reserves, increasing it by $525 million from the end of last year to $1 billion in March.

Forecasting the prosperity of global banks who are deeply vulnerable to the losses of their energy portfolios will be difficult, but can be largely attributed to the wellbeing of the energy sector. Banks will be scrutinising the results that energy companies are bringing out, as their profitability is so dependent on the earnings of the oil and gas producers. BP was the first of the “supermajors” to report their earnings, revealing profits of $532 million, 79 per cent down from the same period in 2015, but also showing a $339 million increase since postings in the previous quarter.

BP’s Exploration & Production (E&P) operations took a toll on their earnings, as the department is costing more than it’s earning. Those who are likely to fare better in the energy sector are those with less exposure to E&P, as this is the area of the industry most affected by oil prices, and those who are well-diversified in their trading. Companies such as Cargill are expected to do well, by turning their attention downstream, moving away from energy-linked businesses.

However, amongst all the souring loans and tumbling oil prices, investors have something to look forward to in the energy sector – the proposed Saudi Aramco IPO. News broke in October last year of plans for an IPO listing of Saudi Arabian Oil Company (Aramco), Saudi Arabia’s state owned oil company, estimating a possible value over $2 trillion. The sale will likely be less than 5 per cent of the company and focus on the sale of their downstream assets i.e. their refinery businesses, as opposed to the parent company, which holds their excessively lucrative crude reserves. Bloomberg analysts have stated that JP Morgan and HSBC are likely to win the IPO as they are the top ranked lenders in Saudi Arabia for IPOs.

Aramco expects the oil supply-demand balance to bring recovery to oil prices by the end of 2016, but this IPO could aid their economy in financing the $98bn budget deficit the Kingdom suffered in 2015. Nevertheless, it remains to be seen what effect this IPO will have on the Kingdom in the long-term. Taking Aramco public is financially desirable, but it’s doubtful that it would have much of an effect on the Saudi royal family’s enormous total wealth. This shows that their thinking goes beyond monetary gain and demonstrates an intention to reduce the economy’s reliance on oil and increase transparency in the Saudi market by publicly announcing earnings. This IPO supposedly plays a small part in “Saudi Vision 2030”, released by Saudi government on Monday, which includes regulatory, budget and policy changes that could result in an overhaul of their economy if the proposed reforms are indeed executed.

Despite difficult market conditions and an oil price crash, banks remain cautiously optimistic about their global markets businesses. They claim sufficient capital has been put in place to cover future losses and that any hits made to their revenues won’t be enough to make much of a dent. First quarter results from energy companies have also been better than anticipated and their resilience could indicate a quicker turnaround in the oil markets than expected. This coupled with the industry providing what will be the world’s biggest IPO, double the size of the Alibaba IPO, could bring the energy sector back to the forefront of the global economy.

In a period where many banks have been selling off their energy businesses, those who chose to keep their assets will be well-positioned to reap the profits if the sector rebounds. During such market uncertainty, it will be interesting to see whether those with the biggest risk appetites will sink or ride the wave to profitable shores.

Hello and welcome to the Fides Weekly Update. We’re here to bring you a breakdown of this week’s most interesting new stories in legal and compliance. Scroll down to see the Movers and Shakers of the week.

This week:

1) Partner Promotions Snapshot: The Story so Far

Promotion season is upon us, with a number of UK law firm’s announcing their latest rounds of promotions this week.

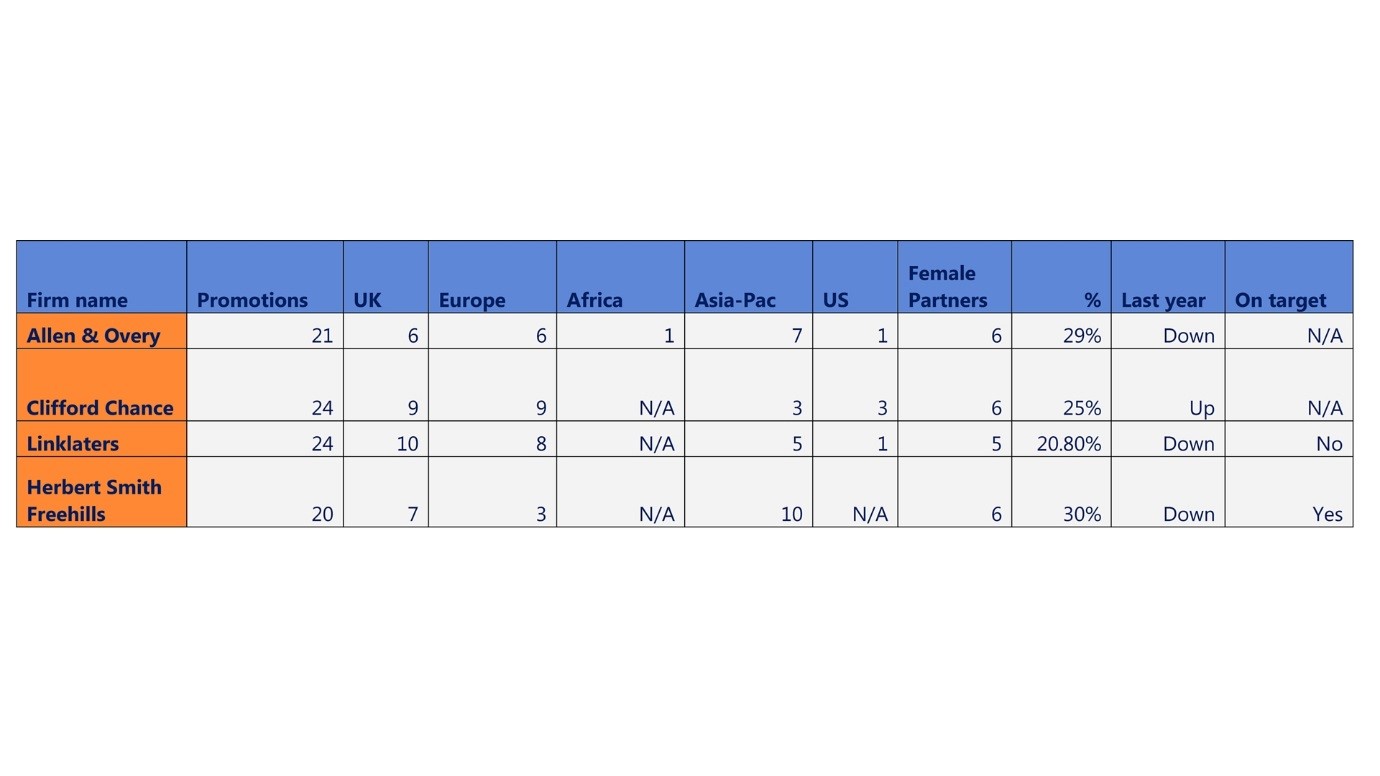

Of the Magic Circle, Clifford Chance and Linklaters announced global promotion rounds of 24, whilst Allen & Overy have made up 21 associates to partner. With 10 partners made up in the city, Linklaters saw the largest number of promotions in London, followed narrowly by Clifford Chance (9) and A&O (6). Whilst promotions were evenly distributed across the UK and EMEA with the former, A&O made up the majority of their partners in the Asia-Pacific in a predominantly banking-focused promotion round. On the other hand, Linklaters favoured its capital markets practice having not made any promotions in this space last year, whilst at Clifford Chance promotions were split evenly across corporate and finance.

The story was similar at global firm Herbert Smith Freehills who announced their latest round of promotions today. The firm made up 20 partners worldwide, including six in Australia and seven in London. Of this, eight were made up into corporate and five into finance. Focus on gender equality has not been far from these announcements, with Clifford Chance and A&O making up six female partners (25% and 29% respectfully) compared to Linklaters five. This was down on last year’s promotion round for A&O, who made up an impressive nine women to partner (40%) in 2015. Herbert Smith Freehills also made up six female partners, putting them in line with the 30% female partnership target they set to achieve in 2019, however this too was down from nine female partner promotions last year.

Focus on gender equality has not been far from these announcements, with Clifford Chance and A&O making up six female partners (25% and 29% respectfully) compared to Linklaters five. This was down on last year’s promotion round for A&O, who made up an impressive nine women to partner (40%) in 2015. Herbert Smith Freehills also made up six female partners, putting them in line with the 30% female partnership target they set to achieve in 2019, however this too was down from nine female partner promotions last year.

This is in contrast to Clyde & Co and Mischon de Reya, who also announced their promotions rounds in the past few weeks. Clyde & Co achieved parity in its number of female promotions, making up eight women in a record-breaking promotions round of 16 new partners. On the other hand, Mischon de Reya made up four female partners in a majority female promotion round, following on from its all-female promotion round in 2015. In 2014 the firm introduced ‘unlimited holidays’ and a new agile working policy in a bid to retain and attract talented female individuals.

At the same time, Macfarlanes were criticised in the legal press for their lack of female promotions, making up no women for the first time in three years. This is in contrast to previous promotion rounds, which have seen a minimum of 30% female partner promotions in recent years. In commenting on the promotions, Senior Partner Charles Martin noted that the round was a “large group by historic standards but one that is uncharacteristically and disappointingly lacking in women.”

In conclusion, it is encouraging that the proportion of women made up into partnership has become a cornerstone of this reporting. However as shown with Clyde & Co and Mischon de Reya, the actualisation of equal or majority female partnership rounds are dependent on the alignment of factors specific to a firms size, practice area focus and internal culture.

For a copy of our article A Path to Parity: Reassessing Gender Balance within UK Law Firms please contact research@fidessearch.com

2) Compliance failings at Mitsubishi Motors

Mitsubishi Motors has suffered another blow to their business due to a failure in compliance, something which the company has struggled to resolve after a number of shortcomings.

This week Mitsubishi Motors Corp. disclosed a manipulation in their fuel economy testing after Nissan found discrepancies in cars provided to them by Mitsubishi Motors. It seems the Japanese carmaker managed to publish improved fuel economy data by flattening their types to bring about lower mileage rates.

Company President Tetsuro Aikawa has been sincerely apologetic about the scandal, saying that although he was unaware of the fraud, he feels responsible. The false data has led to 625,000 cars having to be recalled and Mitsubishi shares plummeting by 33%, as reported by CNN Money.

The company have had an unfortunate history involving such quality lapses and recall failures, spanning over a decade. In 2000, Mitsubishi Motors announced that it had covered up safety defects and customer complaints about its vehicles, which led to the admission of broader problems going back decades and, in turn, the biggest automotive recall scandal of all time.

Mitsubishi’s regulatory compliance and internal oversight have hardly improved since these wrongdoings. The carmaker has failed in reinforcing a compliance culture into the business, something which Aikawa claims has been extremely difficult to instil into all employees. Nikkei Asian Review has remarked that failures in their internal chain of command and poor sharing of information is the root cause of their compliance failings.

This is just the latest scandal to hit the automotive industry, after Volkswagen were caught rigging emissions tests last year. The German carmaker came to an agreement this week with US regulators as part of the settlement regarding their emissions scandal. It was also announced today that fellow German carmaker Daimler, the owner of the Mercedes Benz brand, has begun an internal investigation into the way it certifies diesel exhaust emissions in the US.

Violations of regulatory compliance are a regular occurrence in the automotive industry. Regulators are becoming much more aggressive in enforcing regulatory frameworks and with increasing importance placed on reputational risk and preventing brand damage, carmakers in the industry will have to begin developing better approaches in ensuring compliance standards are met.

Movers and Shakers of the week

Appointments

Ashurst elects Australian managing partner

Finance co-head Paul Jenkins has been appointed the first Australian managing partner at Ashurst, taking over the role from James Collis in June

Royal Mail appoints permanent GC

Royal Mail’s interim general counsel Maaike de Bie has been confirmed as general counsel for the business

Moves

Gibson Dunn bolsters London corporate offering

Financial regulatory partner James Perry exits Ashurst to join Gibson Dunn & Crutcher’s London office

CC hire CMA director in an attempt to rebuild competition team

The UK Competition and Markets Authority’s director of mergers Nelson Jung will join Clifford Chance’s partnership in London, one week after the firm lost competition heavyweight Alastair Mourdant to Freshfields Bruckhaus Deringer

KWM lose two further partners

Darren Rogers and Patrick Williams leave King & Wood Mallesons for Ashurst’s real estate practice in London

Senior CC partner set to join Surrey law firm

Restructuring & insolvency partner David Steinberg is to join Stevens & Bolton, after 22 years as a partner at Clifford Chance

Office Openings & Closings

Central Asian-based firm enters Iranian legal market

Colibri Law has become the second international firm to set up Iran, opening its doors in Tehran

Partner Promotions

Clyde & Co promotes 16 to partnership, five in the City

Linklaters makes up 24 partners, 10 in London

Clifford Chance promotes 24 globally, with nine partners in London

Herbert Smith Freehills makes up 20 globally and seven in London

Hello and Welcome to the Fides Weekly Update. Take a look at which legal and compliance stories our Researchers have been talking about this week. Scroll down to check out the Movers & Shakers of the week.

Contact research@fidessearch.com to subscribe to our weekly newsletter.

This week:

1) Addleshaws considers restrictions on partner exits

Management attempts to limit partner exits through changes to the partnership deed has been met with staunch opposition at Addleshaw Goddard, as reported in Legal Week today.

Partners are divided over the proposed changes to the partnership deed, which would restrict the number of partners able to resign in each financial year to just seven. The proposed changes cover both fixed share and equity partners, and would introduce a ‘bad leavers’ policy that would allow the firm to slash a departing partner’s equity share by up to 30% if they were deemed to be in breach of the agreement.

The firm has been reviewing its partnership articles since November with the arrival of new General Counsel Simon Callander from Olswang. Although the goal was to have the new deed in place by 1 May, management are now said to be “scrambling desperately” to put in more consultations and to persuade the partnership to vote in favour of the proposals.

Whilst the firms’ partnership deed already has a lock-in that is triggered when seven equity partners have handed in their notice in any one year, the new proposals would extend this provision to also include fixed shared partners, further limiting the amount of exits from the firm.

This is somewhat surprising as it comes on the back of strong financial performance by the firm who made up 15 new partners at the start of the month. Last summer, Addleshaw’s saw its top of equity soar 67% to £936,000 after a 12 per cent revenue increase and an 11.6 per cent increase in net profit for the 2014/15 financial year. Changes to the firm’s bonus system also saw the distribution of a firm-wide bonus at the end of 2015, as previously the firm had not often reached the profit level needed to reward its partners.

However, in spite of recent financial success the firm has seen a string of exits over the last few years, including a number of senior figures. Most notably, in December 2015 former Managing Partner Paul Devitt and M&A Partner Richard Thomas joined EY in Manchester, led by ex-Addleshaws corporate Managing Partner Philip Goodstone. More recently, the firm has seen departures from its Real Estate team with practice head Jane Hollinshead moving to IJD Consulting Limited and Asia real estate specialist Helen Worth relocating back to Hong Kong in February. In Dubai, Addleshaw’s also lost M&A partner Ben Gillespie who joined DLA as Head of Corporate for the Middle East.

With internal consultations to the partnership deed still ongoing, how Addleshaw’s management envisage the ‘bad leavers’ policy being realistically implemented across the firm’s 170 fixed shard and equity partners is a question that needs answering. Furthermore, with internal divisions over the proposed change rife, it will be interesting to see how partners react if the decision does not go their way.

2) FCA shine a light on IPO process

FCA published an interim report on the investment banking and corporate market this week. More interestingly, they released a discussion paper alongside this looking into the IPO process and how information is released to investors.

The main conclusion from the interim report is that competition needs to be further encouraged in equity and debt capital markets. It claimed that cross-selling restricts competition for smaller institutions who cannot offer the same lending facilities as their larger competitors. The regulator suggests one way to increase competition in this field is by prohibiting the use of contractual clauses that limits a client’s choice of providers on future transactions, a tool widely used in the market.

Meanwhile, the FCA has released a discussion paper in an attempt to start up a debate on revised practices for IPOs.

Access to information on company flotations and the allocation of shares amongst investors are high on the agenda for the FCA, as there seems to be a lack of transparency around new offerings, especially at earlier stages.

During the IPO process there is a blackout period, typically 14 days, between research on the issuer being published by banks supporting the IPO and the circulation of the issuer’s prospectus. The FCA argue that that investors are receiving such vital information too late into the process, at the point where managers will likely have already made their investment decisions.

The regulator has suggested a new proposal, similar to that of the US, whereby the initial research is delayed until after the issuer prospectus has been released, allowing investors to make a fully informed decision.

It seems this change has been welcomed in the market and many believe it will provide more flexibility when launching a transaction. Morgan Stanley’s co-head of global capital markets Henrik Gobel said: “we have for a long time been a big proponent of having a prospectus filing system similar to the US.”

The findings, which came from the FCA’s assessment of 10,000 deals over a period of five years, also showed that banks tend to make more favourable allocations of shares to investors that submitted price-sensitive bids as well as those who attend meetings with the issuer before the IPO. This conflict of interest will also be investigated in a bid to remove any “potentially anti-competitive practices” in the system. The FCA believe that external researchers and analysts conducting independent research must also be allowed to attend meetings with the issuer’s management. This will improve the quality and depth of independent research and ensure that investors don’t solely make decisions based on material prepared by the syndicate banks’ analysts, who are focused on selling the IPO.

The IPO market itself has suffered a long dry spell over the last year. After several strong years of IPO activity, stock market volatility has weakened investor appetite for high-profile offerings. The value of IPOs fell by 36 per cent between 2014 and 2015, whilst Q1 in 2016 showed that IPOs got off to an even slower start. EY reported a total of 167 deals, raising just $12.1bn last quarter, which represents a 70% decline in total capital raised compared to this time last year. IPO activity has been the weakest since 2009 and with the fear of further global economic slowdown and turbulent market conditions, it is predicted that the M&A market will continue to fare better than the IPO market, as it is less sensitive to potential slowdowns in economic growth and continued uncertainty around the economic environment and the looming Brexit referendum.

Movers and Shakers of the week

Appointments

Clifford Chance announces new Asia Pac head

Geraint Hughes is to replace Peter Charlton in the role of Asia Pacific regional managing partner, beginning in September 2016.

Skadden name NY white collar partner as London enforcement head

Skadden, Arps, Slate, Meagher & Flom have relocated white collar partner Keith Krakaur from New York to London, where he will serve as head of the firm’s European government enforcement and white collar crime practice

Pinsents banking head seconded to Barclays

Michael Isaacs, head of banking & finance at Pinsent Masons, has been seconded to Barclays’ litigation and investigations team

Moves

OneSavings Bank hire interim GC

Martin Purvis has joined OneSavings Bank as interim general counsel to replace Zoe Bucknell, who resigned last month. He previously held the role of interim head of secretariat at Balfour Beatty.

Airbnb hire GC from Ebay

eBay’s vice president and deputy general counsel Rob Chesnut has joined Airbnb as their new general counsel

Ashurst expand global fintech team

Ashurst have appointed David Futter as a partner in their global fintech practice, based in their London office. He joins from Addleshaw Goddard.

KWM lose three partners from London office

IP partner David Rose leaves King & Wood Mallesons for Mischon de Reya, whilst IP partner Campbell Forsyth and commercial partner Gretchen Scott join Dentons and Goodwin Procter respectively.

Mayer Brown expand London finance capability

Dentons finance duo Tom Eldridge and Liz Soutter have joined Mayer Brown’s London office

PwC Legal hire employment partner

Employment partner Tom Kerr Williams departs DLA Piper to join PwC Legal

A&O re-hires TMT and IP partner

Tom Butcher has returned to Allen & Overy to head its Middle East TMT and IP practice. He joins from Simmons & Simmons

Stephenson Harwood boost corporate offering in London

Corporate partner Anthony Clare exits Ashurst to join the London office of Stephenson Harwood

Simmons lose aviation finance duo to US firm

Winston & Strawn have hired aviation finance partners Mark Moody and Christopher Boresjo from Simmons & Simmons in London

Hengeler Mueller lose 3-strong corporate team

Kirkland & Ellis have have taken on M&A partner Achim Herfs, counsel Anna Schwander and senior associate Benjamin Leyendecker-Langer, who will all join the firm as partners. All three depart from Hengeler Mueller’s Munich office.

Linklaters make senior partner hire

Former Allen & Overy real estate head Mark O’Neill has joined Linklaters in their real estate finance team

Orrick take four from Freshfield’s Paris office

Four partners from Freshfields Bruckhaus Deringer will join the Paris office of Orrick Herrington & Sutcliffe. this includes Paris employment head Emmanuel Bernard, finance partners Hervé Touraine and Emmanuel Ringeval and corporate partner Patrick Tardivy

Herbert Smith make disputes team hire in Frankfurt

Herbert Smith Freehills have taken on name partner Helmut Görling and partner Dirk Seiler, along with seven lawyers, from boutique firm Acker Görling & Schmalz (AGS Legal).

BLP re-hires competition litigation partner

Edward Coulson departs from Hausfeld to re-join Berwin Leighton Paisner in their Litigation and Corporate Risk practice.

Partner Promotions

Macfarlanes promotes six to its partnership

Allen & Overy promote 21, making up six in the City

Welcome back to the Fides Weekly Update.

We would like to inform you this week of our recent office move. Fides Search has found a new home at 60 Gresham St, London, EC2V 7BB.

Read on for the week’s top stories along with our regular list of movers and shakers.

Follow us @Fides_Search for the latest headlines in legal and compliance.

This week:

1) ‘Panama Papers’ and its effect in the legal sector

Tensions are high this week as the ‘Panama Papers’ scandal puts many at risk of exposure for dodging taxes, money laundering and evading sanctions.

11.5 million documents were leaked on Sunday from Panama-based law firm Mossack Fonseca and implicate a variety of current and former heads of state, global institutions and the rest of the world’s most rich and powerful, making it the largest data leak in history.

As journalists gradually scour through the mountain of leaked files, the revelations are bringing up a whole host of questions in the legal market.

Firstly, it reignites the debate regarding the ethical implications of tax avoidance as well as the fine line between “aggressive” tax avoidance and illegal tax evasion. Legal Business posted an insightful blog that discusses a shift that took place post-banking crisis, discouraging the use of offshore jurisdictions for tax purposes, and how this scandal will shift this perspective further, placing additional pressure on the morality of law firm clients’ tax affairs.

The leak has also revealed a multitude of allegations regarding money laundering and evading sanctions. The FT reported on Wednesday that 33 companies and individuals listed in the leaked documents are on the US sanctions blacklist, many of whom are guilty of supporting regimes in North Korea, Zimbabwe, Russia, Iran and Syria.

The London property market is also being looked into as the documents show a huge number of London properties are being purchased through offshore companies supplied by Mossack Fonseca. The Guardian has revealed that the prime minister of Pakistan, Iraq’s former interim prime minister and the president of the Nigerian senate are among those whose links to London property appear in the files. These arrangements, although legal, could be dangerous as they allow for large sums of black money to be laundered through the property market. A director at the National Crime Agency aired his views last year, claiming that the London housing market had been “skewed by laundered money”.

In light of the data leak, the Financial Conduct Authority (FCA) has set a deadline for banks to disclose any business conducted with the law firm to ensure no wrongdoing has taken place. A number of global investment banks are featured in the ‘Panama Papers’ requesting the set-up of offshore companies for their clients, including those subject to international sanctions, making it harder for officials to pinpoint money flows. The action taken by the FCA comes days after the organisation released their business plan for 2016/17, which featured a crackdown on financial crime and money laundering as one of their seven priority themes for the year.

Lastly, such a big data leak has highlighted the inadequacy of data security in law firms. Last week we took a look into cybersecurity in law firms, and the impending threat to their outdated systems as it was reported that 48 top US law firms, along with a selection of UK firms, were targeted by a Russian cybercriminal in an attempt to extract confidential client information. The kind of data breech that brought on ‘Panama Papers’ however, has exposed an even larger weakness in law firm security and questions the ability of law firms to protect confidential client data, a fundamental aspect to their businesses.

The vulnerabilities of Mossack Fonseca’s front-end computer systems that were outlined by wired.co.uk will only further put into the spotlight the outdated systems operated by some law firms, leaving many in the sector open to attacks. If a firm that is shrouded in so much secrecy can have over 11 million documents stolen, how easy can it be to access the files of law firms who don’t require such high levels of privacy?

It is clear that there will be fallout in the legal profession as a result of ‘Panama Papers’, both for law firms themselves as well as consequences for their clients. In particular, it seems this scandal could cause the legal industry to begin offering more advice on the ethical ramifications of their deals as reputational risk begins to carry more weight alongside the legal liability of their actions.

2) Cravath lose M&A heavyweight

It is not often that you see the details of a lateral partner move reported in the New York Times, but that is what happened this week when it was announced on Sunday that M&A heavyweight Scott Barshay has joined Paul, Weiss, Rifkind, Wharton & Garrison from Cravath, Swaine & Moore, where he has spent the entirety of his 25 year career.

With Barshay advising on $292 billion in M&A transactions last year, roughly a third of Cravath’s total announced deals for 2015, this is undoubtedly a huge blow for the firm. One of the best-regarded M&A practices in the US, Cravath ranks second only to Skadden according to data compiled by Thompson Reuters, having completed 97 transactions worth $926.5 billion last year. Paul Weiss on the other hand, where Barshay will join as Global Head of M&A, currently rank at 19th in the mergers league tables, working on 142 deals announced last year that were worth $309.3 billion.

Beyond the financial implications, a reason why this move has garnered so much national (and international) attention, is because lateral hires from Cravath are rare. With the majority of partners working at the firm having done so since the inception of their careers, more frequently Cravath partners who’ve left the firm have gone to banks or taken up positions with the government.

As for what motivated the move, the profitability of Paul Weiss (which last year reported its 20th consecutive year of profit increase), and attractiveness of its modified lockstep remuneration system have been well cited.

Despite advising on a record-breaking $927 billion in deals in 2015, revenues at Cravath only rose a modest 2.9 percent to $666.5 million. Paul Weiss on the other hand turned over $1.109 billion in revenues last year, an increase by 7.1 percent from 2014 that saw average take-home profits for equity partnership surge past the $4 million mark for the first time. Under the modified lockstep and sizeable bonus pool at Paul Weiss, opposed to the pure lockstep at Cravath, it also stands that Barshay will be better remunerated at his new home.

However, this overlooks the point Barshay stated for moving; that greater diversity in Paul Weiss’s practice areas offered him a more attractive platform from which to expand his practice. With market leading practices in litigation, private equity and white collar defense, a Global Head position at Paul Weiss offered “such an amazing opportunity for me and for our clients that I couldn’t say no.”

In a sector that remains highly competitive on both sides of the Atlantic, with firm’s modifying their lockstep systems (as we have noted in previous weeks with Freshfields) in order to hang on to and attract star performers, it again raises the question of law firm partnership structures whilst also promoting that successful lateral hires shouldn’t be focused solely on money, but about the importance for partners and firms serving their clients to the best of their ability.

Movers and Shakers of the week

Moves

Paul Weiss hire top M&A lawyer

Scott Barshay has exited Cravath, Swaine & Moore to join Paul, Weiss, Rifkind, Wharton & Garrison as global head of M&A.

KWM lose IP head along with two further partners

Intellectual property head David Rose is to join Mischon de Reya as fellow IP partner Campbell Forsyth joins Dentons. Partner Gretchen Scott also exits the firm to join Goodwin Procter.

Lloyds appoints new GC for group legal

Nathan Butler has been hired from the National Australia Bank where he was general counsel to become general counsel for group legal at Lloyds, a role formally held by Hugh Pugsley.

Squire Patton Boggs boosts financial services capability in Paris

Veronique Collin has joined Squire Patton Boggs, having previously been a partner at Freshfields and DLA Piper.

Mayer Brown adds two partners to its German Banking & Finance practice

Mayer Brown has hired Dr. Martin Heuber and Dr Holger Schelling, joining from Freshfields Bruckhaus Deringer and DZ Bank AG respectively.

White & Case make an addition to their Global Intellectual Property Practice

IP partner Lindsey Canning has joined White & Case from Freshfields Bruckhaus Deringer.

WFW make key hire in Paris

Former De Gaulle Fleurance & Associés partner Arnaud Trozier has moved to Watson Farley & Williams and will sit in their Paris Energy & Infrastructure team.

Simmons adds to financial markets team in Singapore

Simmons & Simmons has appointed Matthew Cox to their Financial Markets practice in their Singapore office. He joins from Dentons.

Fieldfisher partner moves in-house

Banking and restructuring partner Simon Coles has taken on the role of general counsel for cash flow finance provider MarketInvoice.

Freshfields partner launches boutique in Hamburg

Planning and regulatory partner Michael Schaefer has left Freshfields Bruckhaus Deringer and taken three associates with him to launch boutique firm Chatham Partners in Hamburg.

Goodwin Procter launches PE practice in Paris

Six partners have joined Goodwin Procter from King & Wood Mallesons, including KWM’s Paris head Christophe Digoy, to build a french private equity offering.

Office Openings & Closings

Freshfields open second legal services hub

Freshfields Bruckhaus Deringer will launch their second legal services centre in Vancouver to work alongside their current office in Manchester

Partner Promotions

Addleshaw Goddard promotes 15, 13 in the UK

Skadden promotes 11 globally, two in the City

Allen & Overy promotes 21, six in London

Nabarro promotes five partners

Pinsent Masons promotes 18, one in France

Hello and welcome to the Fides Weekly Update. Take a look at this week’s key trends, moves and developments in legal and compliance.

Follow us @Fides_Search for regular market updates and insight .

This week:

1) Cyber Insecurity

Cybersecurity was all the news this week as The Wall Street Journal reported that federal investigators were exploring whether hackers stole confidential information on M&A deals from some of America’s largest law firms.

The breach, which took place at a number of firms last summer including Cravath Swaine & More and Weil Gotshal & Manges, is being investigated by the FBI and Manhattan US attorney’s office to ascertain whether confidential client information was stolen to facilitate insider trading. Where spokespeople from Weil declined to comment, representatives from Cravath admitted that a ‘limited breech’ of its security systems took place, but that the firm was “not aware that any of the information that may have been accessed has been used improperly.”

This came after it was reported on Tuesday that 48 top US law firms – as well as UK firms Allen & Overy, Freshfields Bruckhaus Deringer and Hogan Lovells – had been targeted by a Russian cybercriminal in an effort to extort confidential client information for financial gain. In an attempt to solicit help from other hackers, ‘Oleras’ offered to sell his phishing services on a cybercriminal forum to infiltrate the target firms and use keyword search to locate drafts of merger agreements, letters of intent, confidentiality agreements and share purchase agreements. As well as the list of target firms, he also posted the names, email address and social media accounts for specific employees at these firms, leading the FBI to issue a formal alert to firms about these kind of attacks in recent weeks.

Phishing attacks, where criminals send emails to employees masked as legitimate messages in an effort to learn sensitive information like passwords or account information, have become increasingly common and complex. Instead of widespread spam emails, such attacks are now targeted to specific law firm employees and partners often in the guise of seeking legal representation.

With 13 of 15 most prestigious law firms in America targeted, law firms make attractive targets to cybercrime as they hold trade secrets and other valuable information of their corporate clients and are traditionally understaffed in cybersecurity, compared with large corporations and banks. Furthermore, cyber incidents involving law firms are rarely reported to the authorities as there is no specific regulation directed at law firms requiring them to report data breaches and doing so can result in a huge loss of customer confidence. Clients have also come to realise the cybersecurity risk attached to their external counsel, with many conducting independent assessments of the firms that they hire.

Cybersecurity has long been on the boardroom agenda of law firms both sides of the Atlantic. With the stories reported in the news this week confirming that this threat is far from diminishing, law firms must move beyond acknowledging the importance of cybersecurity to seriously improving their systems and training programs to ensure that they will not become victims of the next breech.

2) Lloyds advance on legal restructuring

This week we saw further job losses for junior lawyers at Lloyds Banking Group, making it the second time this year that the bank has restructured its legal team.

These changes are all a part of the three year strategy Lloyds released in October 2014, which involved plans to cut the bank’s workforce by 9,000 and shut 200 branches over the three year period. Lloyds has not yet released details concerning their most recent job cuts in the legal team, but they have stated that new legal roles are also being created as part of their wider restructuring plan.

The restructuring initiative has affected many divisions within the bank, largely hitting their retail, commercial banking and consumer finance teams. The bank’s legal function in particular, has seen its fair share of job cuts as well as experiencing a host of organisational changes, which has resulted in a revolving door of senior level team members.

It was announced in July last year that Linklaters managing partner Simon Davies was exiting the magic circle firm to join Lloyds in the newly created role of chief people, legal and strategy officer. Following this, litigation general counsel Michael Hartridge was replaced by former JP Morgan EMEA litigation head Wilson Thorburn.

It seems the level of structural changes may not have been very well received amongst legal team members at the bank as this week The Lawyer reported on the results of an internal staff survey carried out at Lloyds. It stated that “a significant majority of both the commercial banking and lending support legal teams responded unfavourably to questions about satisfaction and engagement in their jobs”. It was also mentioned that the results from these teams showed “some of the worst scores in the entire organisation”. Wider restructuring across Lloyds will continue, as they works towards the goal of becoming more digitally focused. The bank is expected to continue to reduce headcount, while investing a total of £1.6bn in digital services and automation.

Movers and Shakers of the week

Appointments

A&O welcomes back corporate partner in the Middle East

Tom Butcher has returned to Allen & Overy after two years at Simmons & Simmons to lead their Middle East TMT and IP practice groups

Linklaters assigns new global restructuring co-heads

Rebecca Jarvis and Richard Bussell have been appointed global co-heads for restructuring and insolvency at Linklaters for a four-year term

Moves

BLP add to international arbitration practice

Ania Farren joins Berwin Leighton Paisner from K&L Gates as a partner in their international arbitration team in London

Ashurst hire TMT duo from Herbert Smith

Ashurst has hired partners Nick Elverston and Amanda Hale from Herbert Smith Freehills. They will be joining the firms global TMT practice

Slater & Gordon’s GC exits

Moana Weir is stepping down as general counsel after two months at the firm

Hogan Lovells adds to two partner team in Australia

Partners Richard Hayes, Scott Harris, Andrew Crook and Ros O’Mally have been hired into Hogan Lovells’ Sydney office, the first major office expansion since it launched with two partners last July.

Sidley takes on seven Kirkland associates

Sidley Austin has hired a team of seven corporate associates from Kirkland & Ellis, paying a signing-on fee of up to £100,000 each

The EU referendum debate looms large as David Cameron attempts to persuade the British public that the United Kingdom is better placed in continuing its membership with the European Union. After many years of heavy regulatory burden and an immigration issue that has escalated and shows no sign of a resolution, does Britain need the EU as much as the EU needs Britain? Last week I listened to a webinar run by Herbert Smith Freehills (HSF) which considered the topic of a Brexit, with the public referendum scheduled for the June 23rd and the implications for leaving European Union for Financial Services Regulation. The UK’s continued participation in Europe after four decades in the bloc has seen a plethora of parties pushing its agenda to leave or remain, seldom has there been such indecision.

Britain has the fifth largest economy in the world and is the fourth largest military power. We play a leading role in international affairs as a prominent member of the G7 one of five permanent seat-holders on the UN Security Council. Britain has the largest share of cross border bank lending globally, the second largest Asset Management industry and the third largest insurance industry. As such, of the 358 global businesses headquartered in Europe, only 80 are located outside of the UK. Our Financial Services sector accounts for almost a quarter of the EU’s financial income and 40% of EU Financial Services exports. This gives rise to the question, while there will undoubtedly be a period of uncertainty as new treaties and trade agreements are negotiated, are we well positioned to thrive once free of the shackles of the European Union?

So what are our alternatives? Should Britain vote to leave, a two year Lisbon Treaty would ensue as we negotiate our (br)exit. As highlighted in the HSF webinar, there are a few obvious routes similar to Norway and Switzerland – who incidentally are included in the top 10 wealthiest nations on Earth – such as joining the European Economic Area (EEA) or European Free Trade Association (ETFA), but none of these routes would cure our immigration crisis and are not seen as particularly viable options as our economy and population differ vastly to the current members.

The Financial Services sector has seen a seismic shift since the financial crisis, leading to severe pressure and workload from the European Commission to implement a raft of regulatory change and new legislation. As a result, the Legal and Compliance professions have seen a huge boom, particularly in compliance – a function previously viewed as a back office afterthought now thrust in to the mainstream media and to the top of any board’s agenda. Should we leave the EU, how would these areas be affected again?

As discussed in the HSF presentation, the UK would continue to take part in the European debate for future regulation albeit with reduced authority and persuasion having decided to leave the EU. We have seen significant growth in areas such as government affairs, EU Policy and lobbying, so what price, if any, will these areas have to pay as a result of a vote to leave?

From our discussions with senior figures in banking and private practice, the general consensus is that a vote to leave would have a huge detrimental effect on the UK economy. Indeed of the 500+ participants of the presentation, 80% voted to stay. High level strategic meetings are taking place now to discuss these issues, but of the 278 global businesses currently located in the UK, commentators fear a mass migration of business out of Britain should we leave the EU. Two thirds of the participants felt their current organisation would stay, which leaves a large number considering relocating. How would this affect our UK economy? Our time zone, language, sophisticated legal system, and high calibre workforce has allowed the country to flourish but that may not be enough to entice global institutions if exit negotiations stagnate or stall.

As you can see, there is much to consider and this review only scratches the surface. Outside of the Financial Services sector, we cannot ignore the underlying political debates currently dominating public consciousness. With immigration issues considered to have become the main argument, and the rise in prominence of minority political parties such as UKIP, this is not just an economic issue but a socio-economic problem. Would leaving the EU solve our immigration issue? Is the nation equipped with all the right facts and information to make the most informed decision come June 23rd? The countdown has begun to what could be the one of the most important decisions in our country’s recent history and only time will tell whether it was the right one.

Is there something we can help you with?

If not right now, we can include you on next weeks' newsletter update?

CLICK HERE